How to Build a Billion-Dollar Energy Company in Africa: The NVIDIA Thesis

Template 2: the chip company that decided its customers were too poor, so it became their investor, their anchor customer, and their bank.

Two weeks ago I told you how a Chicago hedge fund ended up owning gas rigs in a Louisiana town famous for butterflies, and I signed off with a promise: the next template would be stranger than a hedge fund...

I keep my promises. Because Template 2 is a chip company that looked at its customers, decided they were too poor to buy its chips, and responded by becoming their investor, their anchor customer, and eventually something that looks suspiciously like their bank.

If that sounds like financial engineering with extra steps, hold that thought. We will get to the extra steps.

But first, a joke.

Revenue is a Mindset 😂

Revenue, Kuveke explains, is a mindset.

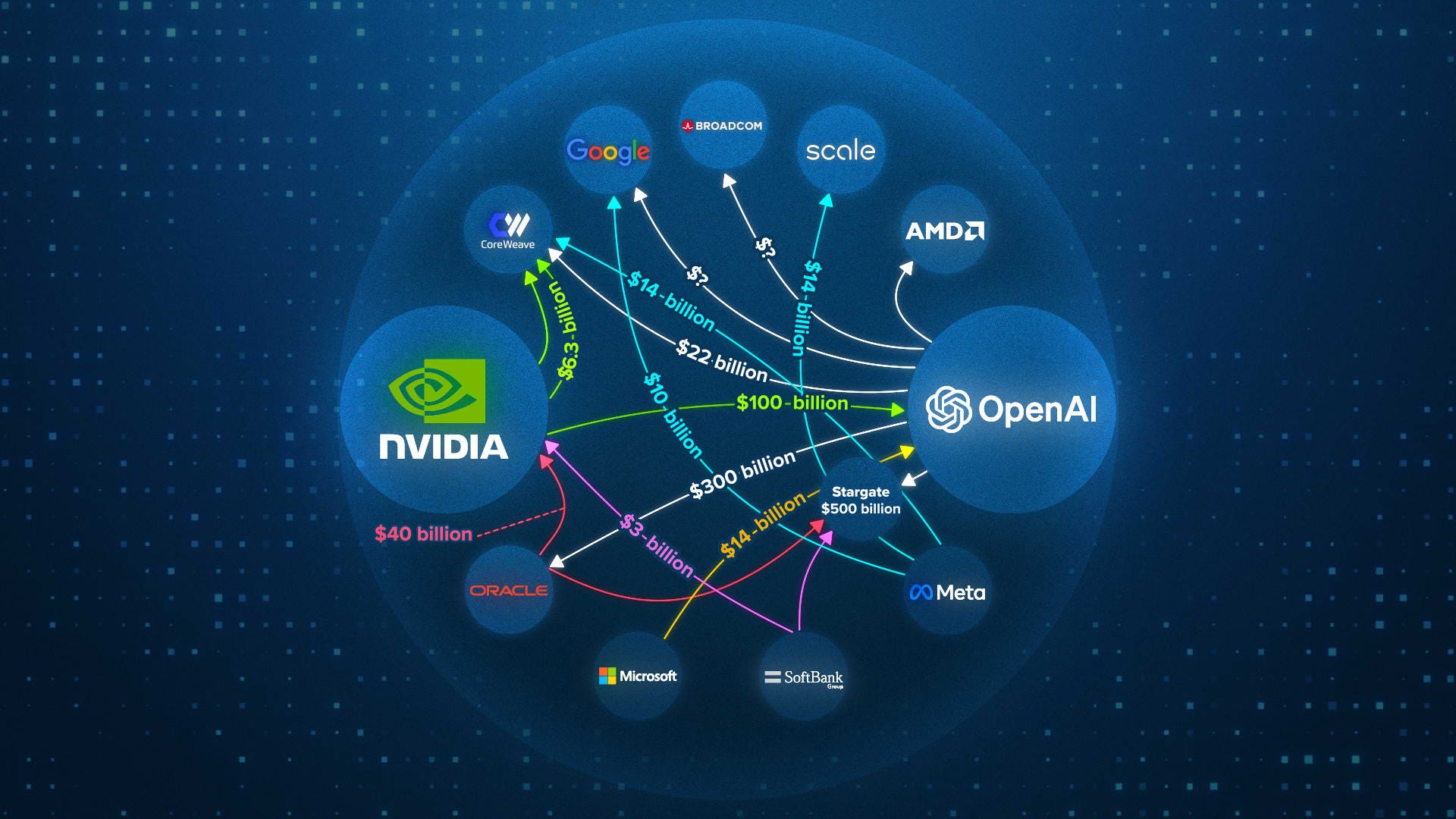

OpenAI commits roughly $300 billion of compute spending to Oracle for cloud capacity (WSJ, Reuters).

Oracle buys mountains of Nvidia GPUs to serve it for tens of billions.

Nvidia announces a letter of intent to invest up to $100 billion in OpenAI (Reuters, Bloomberg).

Money out the front door, orders in through the back, and valuations rising on every corner of the triangle. Michael Burry compared it to Enron and Lucent. Jim Chanos, the man who actually shorted Enron, warned about "arcane financial structures" stacked on top of money-losing companies.

The money goes around the circle, everyone’s stock goes up.

Bloomberg ran a whole feature on the circularity of these deals and whether the trillion-dollar AI boom is partly financing itself (Bloomberg). Serious analysts are genuinely worried, and I want to be careful here: circular financing in AI is an open analyst concern, not an adjudicated fraud. Nobody has been marched anywhere in handcuffs. The deals may all prove out. But the structure of the worry gives us a diagnostic, which is the most useful sentence in this essay:

When the money stops cycling, what remains?

If the answer is “nothing,” you have Kuveke’s mindset revenue. If the answer is “a developer ecosystem, a manufacturing base, standards everyone builds on, and customers who keep paying real money for real things,” you have something else entirely. You have bootstrapped an ecosystem into existence using your own balance sheet as scaffolding.

Meet NVIDIA

Some orientation, for anyone who last checked in on Nvidia around 2016. Nvidia designs the chips that train and run AI models, and it currently trades at around $5.2 trillion. Africa’s entire annual output is roughly three trillion. One company, priced above the yearly production of 54 countries and one and a half billion people.

Sit with that for a moment. I had to.

Nvidia, whatever you think of its stock price, has been running the second play for nearly twenty years. And I think it is the most complete template that exists for building the energy company Africa actually needs.

This is not a copy-Nvidia essay. You cannot copy Nvidia. You do not have $4 trillion of market cap, and if you did you would not be reading a Substack called The Impostor’s Guide to Clean Energy.

This is an essay about extracting the operating logic underneath Nvidia and asking what it looks like when the chips are transformers and meters, the developers are gensets and mini-grids, and the infinite money glitch has to survive contact with a Ghanaian utility’s collections department.

The disclaimer from last time carries over. Nobody on this continent needs to cosplay as the Jensen Huang of Ogbomosho. We are here to study the architecture, not to buy leather jackets.

The five things Nvidia actually did

Nvidia’s playbook is five moves, executed in sequence, over two decades.

Move one: build the platform before the demand exists.

In 2006 Nvidia unveiled CUDA, a software layer that let programmers use graphics chips for general-purpose computing. Almost nobody cared. Wall Street treated it as an expensive hobby for the better part of a decade. Nvidia kept paying for it anyway: libraries, compilers, university curricula, developer tools, whole conferences.

Then deep learning arrived, discovered that graphics chips are accidentally perfect for training neural networks. Today CUDA counts roughly six million developers, every major AI framework treats it as the default dialect, and Nvidia books something like 86 percent of all data-centre GPU revenue. Rivals ship silicon with comparable specs on paper and lose anyway, because two decades of accumulated software means the Nvidia chip performs better in the field, and every engineer already speaks its language.

Readers of the Citadel essay will recognise this move. It is the map. Nvidia drew the map of accelerated computing before there was any traffic to put on it, and now all the traffic consults the map.

CUDA looked like an expensive hobby for a decade and a half before it paid. As an Arsenal supporter, I am professionally trained to respect a long wait for silverware.

Move two: sell the stack, never the component. Nvidia does not really sell you a chip anymore. It sells you a rack, the networking, the software, the orchestration, the whole integrated system, which is how a hardware company sustains gross margins above 70% in an industry where components get commoditized for sport. Value lives in integration. Component sellers compete on price; platform sellers compete on switching costs.

Move three: manufacture your own demand side. By early 2026 Nvidia had deployed over $40 billion in equity into its own ecosystem, including a stake in OpenAI that ended up around $30 billion, plus positions in xAI, CoreWeave, a data-centre developer or two, and, my personal favourite, a glass company. Corning. They invested in glass!!!. (I guess when you are underwriting an entire supply chain, you eventually reach the sand), and a small nation’s worth of other companies whose common feature is that they buy or enable the purchase of Nvidia products. Your customers cannot afford your product? Fund the customers. It sounds circular because it is circular. The question, as always, is what remains when the circle stops.

Move four, the strange one: become the credit enhancer for your own ecosystem. This is the move that made me sit up. The neoclouds, companies like CoreWeave that buy GPUs and rent them out, had a problem: lenders had no idea what a GPU would be worth in four years, so they priced the debt like it was radioactive, north of 10% unsecured.

Nvidia’s response was to backstop them. In September 2025 it signed an agreement to buy up to $6.3 billion of CoreWeave’s unsold cloud capacity through April 2032 (Reuters, CNBC). A take-or-pay floor under utilization. With Nvidia guaranteeing the downside, the same borrowers could suddenly raise secured debt around SOFR plus 225 basis points, call it 5.9%. Sit with that number.

The backstop compressed the cost of capital by four to five percentage points. For an infrastructure business, that is the difference between a viable project and a PowerPoint. And here is why Nvidia could rationally do it when no bank could: Nvidia is the only party on Earth that actually knows what GPUs are worth over time. It sees utilization, resale values, failure rates, the roadmap of the next chip that determines the residual value of the current one. Asymmetric information usually shows up in finance as a reason deals die. Nvidia weaponized it in the other direction. It sold its superior knowledge of its own ecosystem as a guarantee, and got paid for it in ecosystem growth.

Move five: know when the scaffolding comes down. In February 2026, the famous $100 billion OpenAI letter of intent quietly became a $30 billion investment (The Guardian), with Jensen Huang clarifying that the original figure was never a binding commitment (Yahoo Finance). You can read that as retreat. I read it as discipline. Scaffolding is supposed to come down. The companies that died doing this play died because they forgot that part, and we will meet the most famous corpse shortly.

Now I am supposed to shout AI bubble

The most useful book I studied on this was Carlota Perez’s Technological Revolutions and Financial Capital, published in 2002. Perez studied five technological revolutions across two centuries and found the same rhythm every time: an installation period, when speculative finance floods in and overbuilds the new infrastructure amid a bubble; a crash; then a deployment period, when the surviving infrastructure gets put to work by everyone and the actual golden age happens. The railway manias bankrupted investors and left railways. The dot-com crash vaporised trillions and left the fibre that later carried YouTube, and eventually this newsletter to your inbox. Bubbles inside a real technological revolution are wasteful, unfair, and strangely productive. Tulip manias leave nothing. Fibre manias leave fibre.

So my answer on AI is that parts of it will end in tears, and the tears will water something. When the music stops, the test is simple and brutal: look at what remains. Round-tripped revenue leaves a bigger number and a court date. Overbuilt infrastructure leaves infrastructure.

Keep that test in your pocket.

We are about to use it on my side of the world, where the collateral does not rot in three years, and where I will now argue this entire playbook works better than it does in California.

How do all these analogies actually apply to African Energy

In Silicon Valley, revenue is a mindset. In African energy, revenue is a collections problem.

When OpenAI commits $300 billion to Oracle, nobody asks whether OpenAI will physically refuse to pay the invoice while continuing to consume the compute. In African power markets, that scenario has a name. Several names, actually, and case files.

Ghana signed a stack of take-or-pay power contracts in the mid-2010s, then demand undershot and the state found itself paying for capacity nobody used. The distribution utility ECG recovers only around 62% of what it bills, the sector accumulated a shortfall of roughly $12.5 billion between 2019 and 2023, and at one point Karpowership, the Turkish company that literally parks a ship full of generators off your coast, was owed over $370 million. A country was in arrears to a boat.

Nigeria’s version: the bulk trader NBET spent years paying generation companies around 35% of their invoices. The accumulated debt to gencos ran into trillions of naira, and in January 2026 the government moved to settle part of it with a ₦501 billion bond issue, which is what it looks like when a sector’s receivables get so bad they have to be converted into sovereign paper to be believed.

So no, you cannot run Kuveke’s play here. Two Lagos startups buying each other’s services for a million dollars a month would not produce $12 million of ARR. It would produce two unpaid invoices and a very awkward wedding, because the founders are probably cousins.

But look at what those horror stories actually did to the market. They taught every international lender that African power revenue is unknowable, and lenders price the unknowable brutally. That pricing shows up in one number, and that number is the entire game.

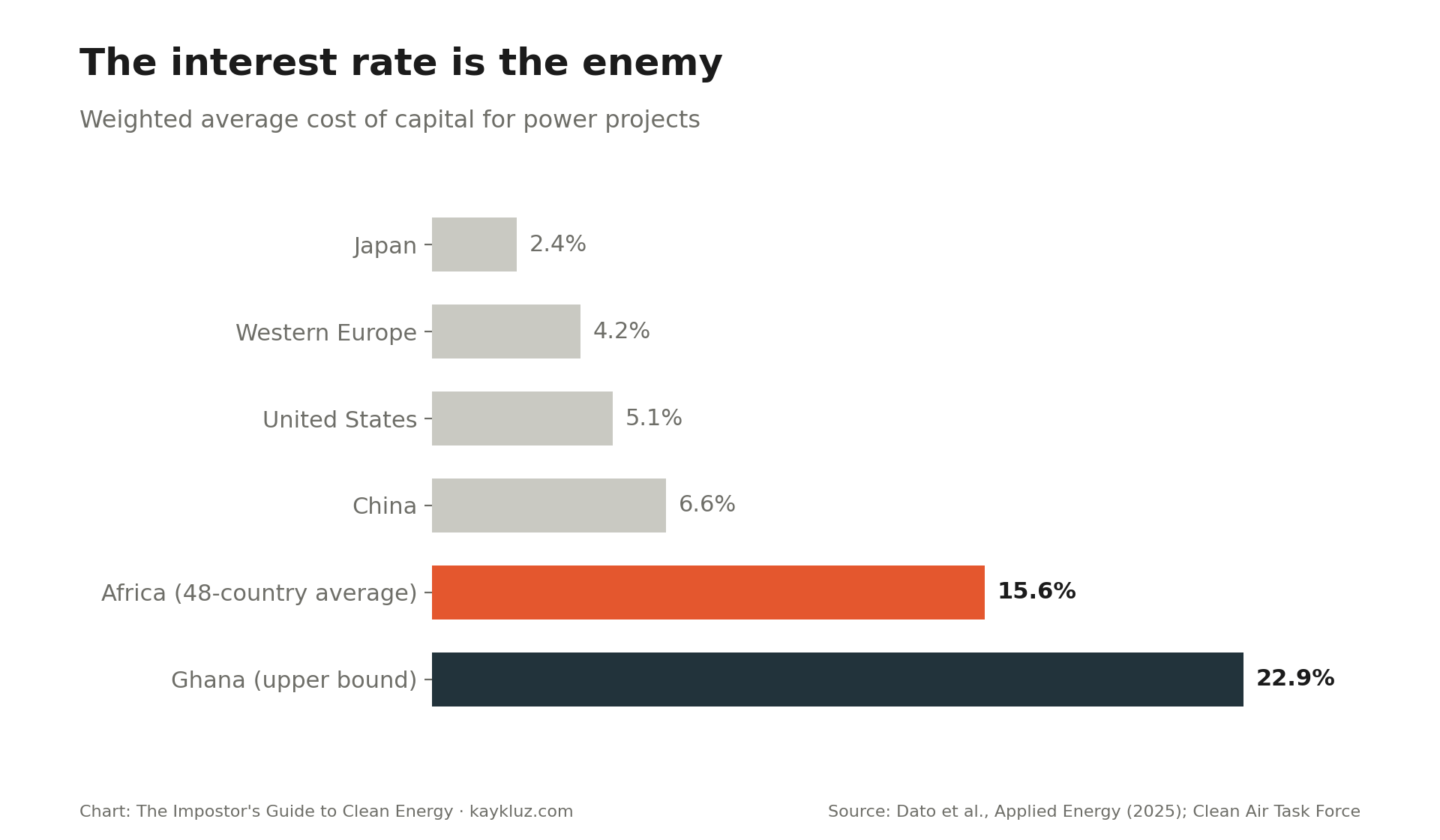

The cost-of-capital spread

A 2025 study in Applied Energy by Dato, Dioha, Hessou and colleagues, working with the Clean Air Task Force across 48 African countries, put the average weighted cost of capital for African power projects at 15.6%, against 5.1% in the United States, 6.6% in China, and 2.4% in Japan (Applied Energy, CATF).

Ghana reaches 20.5 to 22.9%. The sun in Ghana is magnificent. The discount rate is a war crime.

This is why the continent with 20% of the world’s population attracts under 3% of global energy investment, roughly $110 billion of a $3.4 trillion total (IEA World Energy Investment, Africa), while around 600 million people remain without electricity and the World Bank and AfDB scramble to connect 300 million of them under Mission 300.

Solar panels cost broadly the same everywhere. Money does not. The thing we do not have is cheap money

What you actually build

Here is the five-move sequence, translated.

Stage one, the platform before the demand. Build CUDA for electrons. Before the serious capital arrives, someone has to build the instrumentation layer nobody wants to pay for. Meters on factories, cold rooms, telecom sites and mini-grids. Payment histories. Load profiles. Diesel burn. Outage logs. Degradation curves by panel brand, by battery chemistry, by city. The last essay called this the map and spent four thousand words on it, so today I will only add the Nvidia corollary: the map must be built before the market arrives, it will look like an expensive hobby for years, and that is precisely the point. Moats grow in the dark.

Stage two: sell the stack. Do not sell panels. Nobody here buys components either. The African industrial customer does not want panels. He wants his factory to run through the afternoon and his diesel bill to die quietly. The winners already sell exactly that: power as a service, financed, installed, operated and metered under one contract. Daystar Power was doing it across West Africa when Shell bought the whole company in 2022, and its installations now include a 4.2 megawatt system at Nigerian Breweries and a string of Nestlé plants across three countries. CrossBoundary Energy runs the model continent-wide with an awarded portfolio around $700 million, including my favourite deal in African energy: 222 megawatts of solar and a 526 megawatt-hour battery built to feed the Kamoa-Kakula copper mine in the DRC thirty megawatts of clean baseload, around the clock, in one of the hardest operating environments on earth.

Recurring kilowatt-hour revenue against contracts that run ten to twenty years, instead of one-off construction margins. Teece's law again: the profit pools around the complementary assets, the financing, the operations, the relationship, and never around the hardware.

Sell electricity, uptime, cold storage that works, milling that happens, an outcome with an SLA. Integration margins survive commoditization. Component margins do not.Stage three: manufacture the demand side. Nvidia’s equity stakes translate here as anchor offtake. Nvidia converts speculative chip demand into bankable demand by writing cheques into its own customer base. The African energy version is less exotic and frankly more elegant: the anchor offtake agreement. A fifteen-year contract with a brewer, a cement plant, a mine or a tower company, some entity with a hard-currency parent and a treasury that answers emails, does for a power project precisely what Nvidia's $30 billion does for OpenAI. It converts a speculative asset into a financeable one before construction starts. And the newest anchor class arriving on the continent is, pleasingly, the data centre itself, with African capacity headed from around one and a half gigawatts toward two and a half by 2030. Anchor first, then aggregate the smaller loads around the anchor. Never generation first. Generation without offtake is a monument.

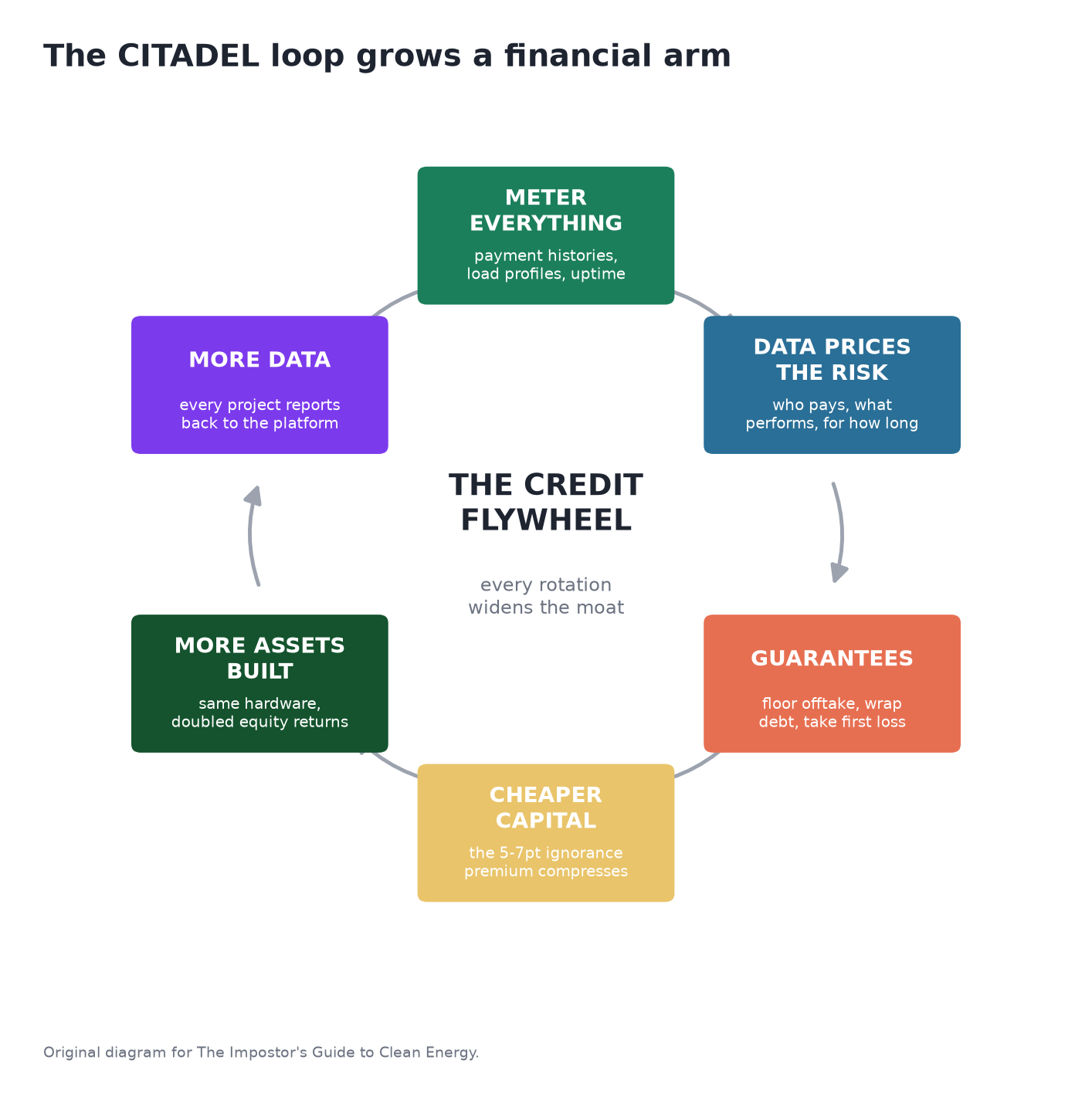

Stage four, the crown jewel: become the credit enhancer. Everything above is prologue. My actual claim is that the billion-dollar African energy company is the one that runs Nvidia’s fourth move. It takes the ignorance premium, those five to seven points of WACC priced off unanswerable questions, answers the questions at portfolio scale, and stands behind the answers with a guarantee.

The astonishing part is that every component of this machine already exists on this continent. They are lying in separate rooms.

In Lagos there is InfraCredit, set up in 2017 by GuarantCo and Nigeria’s sovereign wealth authority, which wraps naira infrastructure bonds in an irrevocable, locally AAA-rated guarantee so that Nigerian pension funds can buy them. It works well enough that it listed its own shares last year and is being cloned in Pakistan and Kenya. That is the wrapper: proof that credit enhancement turns African infrastructure into paper that institutions will hold. (InfraCredit, World Bank PPP).

In Nairobi, in July 2025, Sun King closed $156 million of securitised debt backed by nothing more exotic than the repayment behaviour of about 1.4 million Kenyan solar customers, with Absa, Citi, Co-operative Bank, KCB and Stanbic taking the senior notes and development banks holding the mezzanine. It was the largest securitisation ever completed in sub-Saharan Africa outside South Africa. M-KOPA has raised over $200 million against similar collateral. That is the converter: proof that granular African payment data, gathered meter by meter, transforms directly into cheap senior capital.

And in Washington, that same month, MIGA, the World Bank’s political-risk insurer, executed a $495 million guarantee framework covering up to one hundred CrossBoundary distributed-energy projects at once. (MIGA). Portfolio-level cover, replacing the old one-project-one-negotiation grind. That is the rented balance sheet: proof that the multilaterals will now wrap African energy platforms wholesale.

A wrapper. A converter. A rentable balance sheet. Nvidia’s backstop, disassembled, its parts scattered across three cities, every part already functioning, waiting for the company that bolts them together.

Picture that company. It operates distributed energy assets across half a dozen countries, which is move two. It has metered everything obsessively for a decade, which is move one, so it holds the continent’s deepest verified dataset on the only two questions the ignorance premium is made of: do the offtakers pay, and do the assets perform. Then comes the Nvidia move. It starts underwriting other people’s projects. It issues floor guarantees on portfolios of commercial and industrial solar the way Nvidia guarantees GPU utilisation, wrapped in DFI counter-guarantees the way InfraCredit borrows sovereign trust, and it takes a spread for standing behind numbers it alone can verify.

Nvidia can write its backstop because it authors the roadmap that sets its collateral’s residual value. The African platform can write its backstop because it holds ten years of metered truth about offtakers and assets that no bank possesses. The same asymmetry, on different collateral. The bank prices fear. The platform prices knowledge. The spread between fear and knowledge is the product.

And the arithmetic transfers with indecent precision. Compress a portfolio’s cost of capital from 15 percent toward 9 or 10, territory the best guaranteed African deals already reach, and you have roughly doubled the equity return on identical hardware, the same violence the backstop performed on CoreWeave’s margins. Then the flywheel closes. Every guaranteed project reports its operating data back to the platform. The data sharpens the underwriting. The underwriting strengthens the next guarantee. The guarantee attracts cheaper capital. The capital builds more projects. The projects produce more data. Around and around, widening with every turn.

Now take out the test from the bubble section, because this is where Kuveke’s joke finally gets its answer. Stop the music on the fake flywheel and nothing remains except a bigger number and litigation. Stop the music here and what remains is a twenty-year power asset, metered and contracted, feeding a factory that needed it, plus a dataset that appreciates with age. Nvidia’s collateral is landfill in four years. Ours hums for two decades. The African version of this playbook rests on better collateral than the original.

Stage five: sunset discipline. Write the scaffolding-removal triggers before you write the first guarantee. My proposal: if a backstopped project cannot refinance into ordinary market debt within 24 to 36 months, the demand was never real and the guarantee must shrink, not grow. Nvidia walking its $100 billion LOI back to $30 billion looked embarrassing and was actually the healthiest thing in the whole saga. The alternative is the Lucent ending, and the Lucent ending deserves its own section, because it is the ghost that should haunt every founder who reads this far and feels excited.

The ways this kills you

Lucent Technologies, the pride of Bell Labs, spent the late 1990s vendor-financing its own customers: lending money to upstart telecom carriers so they could buy Lucent equipment, with commitments that reached about $8.1 billion. Revenue looked spectacular right up until roughly 47 of those carriers went bankrupt between 2000 and 2003, at which point Lucent discovered it had been booking its own loans as demand. Revenue collapsed from around $38 billion to $8 billion and the company only survived by merging with Alcatel (American Affairs, MIT Technology Review); Tom Tunguz has a sobering (comparison of Nvidia’s exposure to the Lucent and Nortel playbooks). Same play as Nvidia. Same mechanics. Opposite ending. What separated them was discipline and information: Lucent financed anyone with a pulse and a purchase order, and its only informational edge over its customers’ lenders was superior desperation.

So, the failure modes, stated plainly, because this series has a policy of telling you how the hero dies:

You backstop vibes instead of data. If your guarantees are priced off optimism rather than years of verified payment behavior, you are Lucent with better weather. The whole edge is informational. No data layer, no business.

Your balance sheet is a rounding error at the wrong moment. Nvidia backstops CoreWeave from atop a fortress. You will be making guarantees from something closer to a bouncy castle. This is the most speculative leg of the entire thesis, and I will say it in bold so nobody accuses me of burying it: **operator data alone does not fully substitute for an AA balance sheet.** The honest version of stage four is done in partnership, your data plus InfraCredit’s or GuarantCo’s or MIGA’s capital, with you taking a sliver of first-loss and a slice of the economics. Solo heroics here are how you become a cautionary LinkedIn carousel.

The take-or-pay trap. Ghana’s crisis was caused by take-or-pay commitments detached from real demand. Your stage-three anchor offtakes are take-or-pay commitments. The instrument that saves you is the instrument that killed Accra’s balance sheet. Respect it accordingly, and size every floor against demand you can verify rather than demand you can forecast after two Guinnesses.

The commodity layer commoditizes underneath you. When DeepSeek released open-weight models at a fraction of the incumbents’ costs, the panic was instructive: if the expensive layer gets cheap, who keeps the margin? Solar-plus-storage is on the same curve; panels and cells get relentlessly cheaper. If your business is selling the commodity, the cost curve is coming for you. If your business is distribution, verified data, integration, and cheaper capital, the cost curve is your best salesperson. Cheap hardware plus expensive money is still an unbankable project. You sell the money part.

Political weather. A single regulation on guarantee structures, a currency crisis, a new minister with opinions about foreign-linked credit enhancers, and stage four freezes for a year. Local-currency structures like InfraCredit’s exist precisely because of this. Copy the homework.

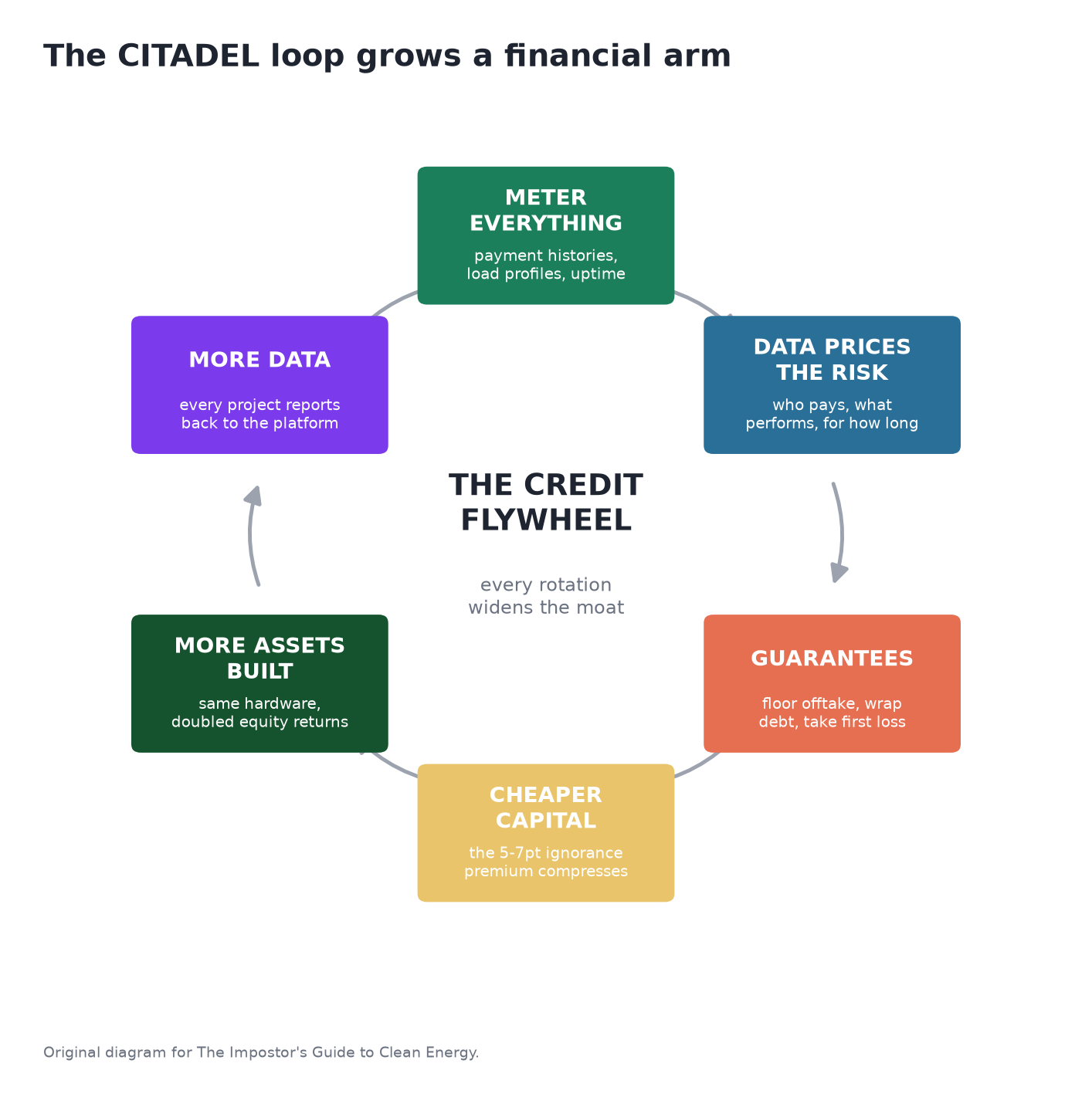

Why this is hard to copy, and the endgame

Recall the CITADEL loop from the last post: the map tells you where to build, the assets generate returns and better data, the merchant layer monetizes the flexibility, and each turn of the loop makes the next turn cheaper. The Nvidia thesis is what happens when that loop grows a financial arm. The map and the meters produce the data. The data prices the risk. The priced risk becomes guarantees. The guarantees cut the cost of capital. The cheaper capital builds more assets, which produce more data. Around and around, and every rotation widens the moat, because a competitor arriving in year five is up against your five years of payment histories and the basis points those histories are worth, and there is no procurement process for that. Panels can be bought. Longitudinal collections data on ten thousand African offtakers cannot, at any price, on any timeline shorter than the one you already traveled.

The endgame, then. The billion-dollar African energy company will not look like a company. It will look like an ecosystem of mutually reinforcing platforms, a data layer, an integrated power operator, a portfolio of anchor demand, and a credit-enhancement arm, each one de-risking the others’ capital expenditure, the whole thing worth more than the sum because the whole thing is the reason each part can borrow. From the outside it will be confusing. Analysts will draw circular diagrams of it and mutter about related-party transactions, and the diligence question will be the same one we started with: when the money stops cycling, what remains? The answer had better be: meters that read, plants that run, mills that pay, and a loan book priced off truth.

Twenty percent of humanity, three percent of the investment, six hundred million people in the dark, and a five-to-seven-point ignorance premium sitting there like free money for whoever does the unglamorous decade of homework first. Jensen Huang built a $4 trillion company by knowing what his ecosystem’s assets were worth when nobody else did. The African version starts smaller, with a meter, a mobile-money receipt, and the radical proposition that a paying customer in Kisumu, properly measured, is a better credit than a hyperscaler’s letter of intent.

Next in the series, we go from strategy to anatomy. If the CITADEL post was the map and this one is the money, the next one is the machine: what the first vertical of this ecosystem actually looks like at ground level, and why it starts in the least glamorous corner of the market on purpose. Wear boots.

- S

P.S. - Nothing here is investment advice. If you lose money backstopping a maize mill because a Substack told you to, that is between you and your risk committee.

P.P.S. - The views are mine alone. Not my employer's, not any board's, and certainly not the investment committee that reads my actual models, who are, for the record, wonderful people with excellent judgment of whom I am not afraid at all.

P.P.P.S. - Long-time readers will suspect, correctly, that this template describes a company that looks a great deal like the one I have been building on nights and weekends. The data layer comes first. It always comes first. Ask the CUDA engineers who spent a decade being asked when they would get a real job.

P.P.P.P.S.- To be scrupulously fair to Nvidia one more time: the circular-financing worry is an analyst concern, not a finding. The commitments are mostly non-binding letters of intent, the totals are not additive, and the company may well be vindicated. Lucent, on the other hand, was adjudicated by reality. Learn from the second one while watching the first.

P.P.P.P.P.S.- Again, none of this is investment advice. I model energy projects for a living, and some of the most beautiful models I have seen ended up face down in the mud because someone forgot that customers, currencies, regulators, and batteries have free will.

Read this as research. Read it as strategy. Read it as vibes. Read it as me, once again, thinking too loudly on the internet.

Sources and further reading

The meme, and the diagrams underneath it

Robin Wigglesworth and colleagues at Bloomberg mapped the circular deals first: “OpenAI’s Nvidia and AMD deals boost $1 trillion AI boom with circular deals,” Bloomberg, October 2025. https://www.bloomberg.com/news/features/2025-10-07/openai-s-nvidia-amd-deals-boost-1-trillion-ai-boom-with-circular-deals

Jack Kuveke’s LinkedIn oeuvre, filed under Jabroni Capital. Consume responsibly.

The Nvidia playbook

CNBC, “CoreWeave stock jumps on disclosure of $6.3 billion order from Nvidia,” September 15, 2025 (the original backstop, obligated through April 2032). https://www.cnbc.com/2025/09/15/coreweave-stock-jumps-on-disclosure-of-6point3-billion-order-from-nvidia.html

NVIDIA corporate blog, “The AI Compute Partnership,” July 2026 (the formalised backstop programme, co-signed by CFO Colette Kress; Sharon AI and Firmus as first adopters).

SemiAnalysis, on AI debt markets, July 7, 2026 (backstopped pricing near SOFR plus 225 basis points against roughly 10 percent unsecured; the projection of more than $7 trillion of AI debt outstanding by 2029).

CNBC, May 9, 2026, on Nvidia’s more than $40 billion of AI equity investments in the first four months of the year, led by the $30 billion OpenAI position.

Wall Street Journal, January 2026, on the Nvidia-OpenAI letter of intent cooling; Bloomberg’s coverage of Jensen Huang at the Morgan Stanley TMT Conference, March 4, 2026 (”might be the last time”).

NVIDIA’s own CUDA twentieth-anniversary materials (roughly six million developers); Mizuho estimates of data-centre GPU revenue share, via Forbes.

Epoch AI, on hyperscaler capital expenditure crossing operating cash flow around Q3 2026; Financial Times and Goldman Sachs compilations of the $725 billion 2026 capex guidance.

The ghosts

Lucent Technologies, Form 10-K for fiscal year 2000 (customer financing commitments of up to $8.1 billion), together with the standard histories of the 2000 to 2003 telecom carrier bankruptcies. The single best cautionary tale in vendor financing.

The theory shelf

Carlota Perez, Technological Revolutions and Financial Capital: The Dynamics of Bubbles and Golden Ages, Edward Elgar, 2002. The book that explains why some bubbles leave railways behind and others leave nothing.

David J. Teece, “Profiting from Technological Innovation: Implications for Integration, Collaboration, Licensing and Public Policy,” Research Policy, Vol. 15, No. 6, 1986, pp. 285-305. https://www.sciencedirect.com/science/article/abs/pii/0048733386900272

Michael G. Jacobides, Carmelo Cennamo and Annabelle Gawer, “Towards a Theory of Ecosystems,” Strategic Management Journal, Vol. 39, No. 8, 2018 (the co-specialised complements argument, for those who want the DFI point in academic dress).

The African cost of capital

Clean Air Task Force, “Evaluating the Weighted Average Cost of Capital (WACC) in the Power Sector for African Countries” (the 15.6 percent average across 48 countries, with some above 25 percent). https://www.catf.us/resource/evaluating-weighted-average-cost-capital-wacc-power-sector-african-countries/

The peer-reviewed version: Dato et al., “Computation of weighted average cost of capital (WACC) in the power sector for African countries and the implications for country-specific electricity technology cost,” Applied Energy. https://www.sciencedirect.com/science/article/abs/pii/S0306261925010633

IEA, Cost of Capital Observatory (the two-to-three times premium, and the decomposition showing the country base rate at 60 to 90 percent of WACC in developing markets). https://www.iea.org/reports/cost-of-capital-observatory

IEA, World Energy Investment 2026, Africa chapter (the roughly $110 billion, the 3 percent share of global energy investment against 20 percent of world population, and the comparison with the more than $105 billion invested globally in data-centre energy infrastructure in 2025).

The disassembled machine

Citi press release, “$156M Sun King Securitization to Deliver Solar for Over a Million Kenyans,” July 2025 (the largest securitisation completed in sub-Saharan Africa outside South Africa; senior notes held by Absa, Citi, Co-operative Bank, KCB and Stanbic). https://www.citigroup.com/global/news/press-release/2025/citi-sun-king-securitization-deliver-solar-million-kenyans

MIGA, “CrossBoundary Energy C&I Africa Portfolio,” the $495 million portfolio guarantee framework covering up to one hundred projects. https://www.miga.org/project/crossboundary-energy-ci-africa-portfolio

CrossBoundary Energy, “$200M senior debt to further renewable energy portfolio in Africa,” November 2025 (the Standard Bank-led facility, and the Kamoa Copper solar-plus-storage baseload deal). https://crossboundaryenergy.com/crossboundary-energy-secures-us200m-senior-debt-to-further-renewable-energy-portfolio-in-africa/

PV Tech, “Shell acquires African C&I solar provider Daystar Power,” December 2022. https://www.pv-tech.org/shell-acquires-african-ci-solar-provider-daystar-power/

InfraCredit Nigeria, established 2017 by GuarantCo and the Nigeria Sovereign Investment Authority; listed on NASD in April 2025, with sister vehicles InfraZamin in Pakistan and Dhamana in Kenya.

The cautionary tales

Ghana’s Energy Sector Recovery Programme documentation and associated World Bank reporting (the $12.5 billion 2019 to 2023 shortfall estimate and the PPA moratorium), plus Ghanaian press reporting on Karpowership’s outstanding receivables, February 2025.

Nigerian reporting on the ₦501 billion NBET bond issuance of January 27, 2026, and Association of Power Generation Companies statements on invoice settlement rates.

And the one that started the series

The Impostor’s Guide to Clean Energy, “How to Build a Billion-Dollar Energy Company in Africa - The CITADEL Thesis,” June 2026. Read it first if you have not. Today’s essay stands on its shoulders