The Foundry Problem (Part 2): What Semiconductors, Oil Barons, and Telecom Towers Can Teach African Energy

Every structural problem the African energy sector faces has been solved somewhere else. The answers are sitting in history books.

In Part 1 of this series, I laid out what is actually killing small renewable energy developers in West Africa: not a bankability problem, but a capital stack mismatch so severe that even good projects die before they can prove themselves. Africa’s average cost of capital for renewables is 15.6% versus Europe’s 2 to 5% range, per the Clean Air Task Force. The identical solar park costs €135/MWh here and €86/MWh there. Same sun. Different architecture. The IEA’s Clean Energy Investment for Development in Africa report puts the base rate at 60-90% of WACC for solar PV in Africa, versus 35% in China and 10% in advanced economies.

This piece is about what history says to do about it.

Here is something I find genuinely clarifying: almost every structural problem this sector faces has been solved somewhere else, in a different industry or a different era, with a different set of actors. The solutions are not hidden. They are sitting in case studies and corporate histories that the African energy sector largely ignores because it is too busy attending conferences about blended finance instruments.

There is a name for what we are experiencing. The economist Carlota Perez studied five technological revolutions over more than 200 years and found a recurring pattern: an installation phase where infrastructure is built through bubbles, speculation, and financial experimentation, followed by a deployment phase where broad societal adoption happens and the real economic gains materialise. The transition between the two, what Perez calls the turning point, requires institutional innovation. Policy. Shared standards. Market-making infrastructure.

The global renewable energy sector is in that transition right now. Solar costs have collapsed. Deployment is beginning at scale in India, Brazil, China, the US. But Africa is attempting to enter the deployment phase without having built the installation-phase institutions. Each African developer must individually traverse both phases, which is structurally impossible for small firms.

Mariana Mazzucato’s complementary framework sharpens the point further. Mazzucato distinguishes between “market fixing” and “market shaping”. The conventional DFI approach to African energy is market fixing: de-risk individual projects, provide concessional capital, correct specific market failures. What the sector actually needs is market shaping: building the institutions that create a functioning market where one does not yet exist. The foundry is not a risk mitigation instrument. It is a market creation instrument.

* * *

The Cleantech 1.0 Autopsy: We Have Seen This Movie Before

Between 2006 and 2011, US venture capital firms poured over $25 billion into clean energy startups. They lost more than half of it. MIT’s Energy Initiative found that more than 90% of cleantech companies funded after 2007 failed to return initial capital to investors.

The post-mortem was devastating. VC firms had expected clean energy to follow the software playbook. Rapid iteration, hockey-stick growth, quick exit. What they got instead was capital-intensive manufacturing, ten-year development timelines, commodity products with razor-thin margins, and dependence on government subsidies that could evaporate overnight.

Van den Heuvel and Popp, in NBER Working Paper 29919, found something that should be tattooed on the forehead of every energy VC: clean energy firms struggled to generate outsized profits because of difficulties differentiating products and increasing market power.

Translation: solar panels are solar panels. You cannot 10x your price because your brand is cooler.

Bessemer Venture Partners did the retrospective in November 2022, analysing 394 cleantech companies via Pitchbook. During Cleantech 1.0, 90% of companies failed to return capital to investors. The survivors added software and services layers. Opower survived by wrapping energy efficiency analytics around utility relationships. First Solar survived by being disciplined: low leverage, strong balance sheet, proprietary cadmium telluride thin-film technology that actually differentiated it from commodity silicon.

SunEdison did the opposite. Aggressive growth. A yieldco model that loaded the parent with $214 million in interest expenses in a single quarter while spinning off operating assets. It filed for bankruptcy in April 2016. Solyndra received a $535 million Department of Energy loan guarantee and still went bankrupt when Chinese manufacturers drove down crystalline silicon costs. Technological novelty is not a moat in commoditised energy hardware. Neither is government-backed capital, by itself.

The lesson is not subtle: clean energy is an infrastructure category, not a venture capital category.

VC works for technology risk. Will this thing work?

Clean energy’s primary risk is deployment and financing. Can we build and sell it at scale?

Those are different risk profiles requiring different capital structures.

And yet here we are in 2026, watching African solar developers try to raise equity from investors who expect software returns on infrastructure timelines. The African tech funding boom saw startups raise approximately $4 to $5 billion in 2021. Then the correction hit. The naira collapsed. Many died. But the ones that survived, Moniepoint, Flutterwave, Paystack, did so because they had built recurring revenue on infrastructure, not because they had the best pitch decks. The lesson for energy is the same.

The lesson: your overhead should be funded by services. Energy audits, feasibility studies, O&M contracts, licensing consulting. Not by project hopes. Build cash flow first, deploy capital later.

* * *

The Semiconductor Analogy

I keep coming back to semiconductors because the structural analogy is almost perfect.

Before the 1990s, the semiconductor industry was dominated by Integrated Device Manufacturers. Companies like Intel, Texas Instruments, and Motorola that did everything: designed chips, built the fabrication facilities to manufacture them, sold the finished product. This worked when fabs cost a few hundred million dollars. It stopped working when fabs crossed a billion. Today, a state-of-the-art TSMC fab costs $20 billion or more. The cost trajectory only makes the foundry model more important over time, not less.

In 1987, Morris Chang founded TSMC with a radical idea: separate chip design from manufacturing. Instead of every company building its own fab, TSMC would manufacture chips for anyone. This single innovation created an entirely new category: the fabless semiconductor company. Qualcomm, NVIDIA, Broadcom, and eventually thousands of others could focus entirely on chip design without needing billions in manufacturing capital.

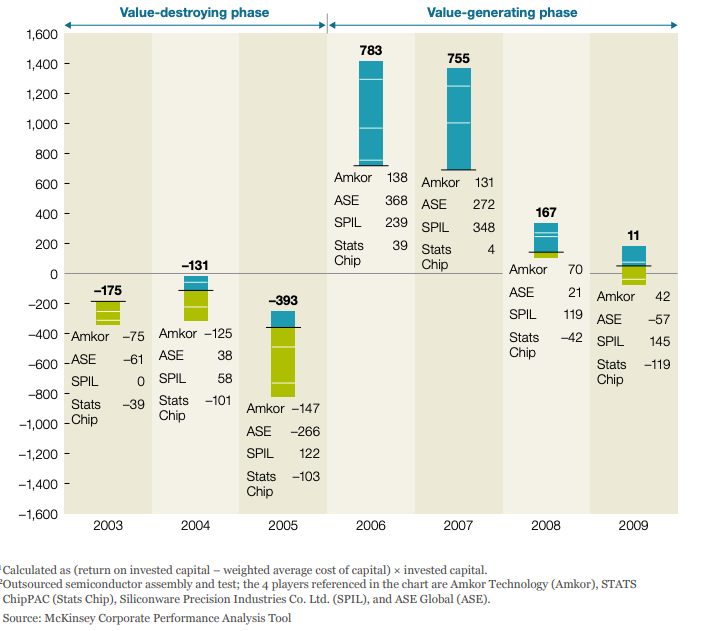

TSMC now holds nearly 70% of global foundry revenue. The scale effect of the dedicated foundry model in semiconductors demonstrates what one well-designed shared infrastructure institution can achieve. IDM market growth stagnated at 1% to 4% CAGR between 2007 and 2024, while the fabless market is projected to grow at 9.6% annually through 2032 per SNS Insider. A McKinsey analysis by Naeher, Suzuki and Wiseman covering 1996 to 2009 found that semiconductor players destroyed a combined $140 billion in value, with most IDMs netting out at zero. The winners were Intel, Texas Instruments, and TSMC. Everyone in the middle got crushed.

Sound familiar?

Right now, most African renewable energy companies are trying to be IDMs. They originate projects, develop them, arrange financing, manage EPC, then operate and maintain the assets. The economist Oliver Williamson, in his 2009 Nobel lecture, explained why this happens. When market-based transactions are too costly, due to incomplete contracts, asset specificity, and information asymmetries, firms vertically integrate. In developed energy markets, a developer can outsource legal counsel, financial advisory, environmental assessment, and technical review to specialist markets. In Africa, these specialist markets barely exist. Every project requires bespoke legal structures. Lenders cannot assess risk without comparable-transaction track records. Regulatory uncertainty makes contracts incomplete by design.

The Williamson-consistent response is vertical integration. But vertical integration has overhead costs prohibitive for small firms. This is the IDM trap.

The contrast with Samsung is instructive. Samsung operates as both chip designer and chip manufacturer, creating inherent conflicts of interest. Fabless customers like NVIDIA and Qualcomm have expressed concern about IP leakage when manufacturing at Samsung Foundry. Samsung is under sustained pressure to spin off its foundry business precisely because trust is critical in the foundry business. The mapping to African energy is direct: state utilities that both buy power as offtaker and compete with IPPs as developers are Samsung, not TSMC. They create the same conflict-of-interest trap. The foundry model requires institutional separation.

Here is the part most people miss about the TSMC story: government capital was decisive. Taiwan’s National Development Fund took a 48.3% stake. Philips invested approximately 27.5%. The government recruited Morris Chang from the US, built the research infrastructure through ITRI, and offered tax benefits that de-risked the entire venture. Five factors drove Taiwan’s semiconductor vertical disintegration: industrial clustering, fast technology change, rising development costs, emergence of design firms, and government support. Remove any one and TSMC probably does not happen.

The African RE sector has the first four. It emphatically lacks the fifth.

The lesson: separate what needs scale from what needs knowledge. EPC, equipment procurement, financing, asset ownership reward scale. Origination, community engagement, regulatory navigation, demand aggregation reward local knowledge. Small companies should own the knowledge-intensive functions and partner for the capital-intensive ones.

* * *

The Seplat Story

The question I get most often is some version of: Seplat and Oando started small and became major players in oil and gas. Why can’t renewable energy developers do the same?

It is the right question. And the answer is instructive precisely because most people cite it incorrectly.

Seplat was formed in 2009 as an SPV. Its founders, through Platform Petroleum and Shebah Petroleum, had spent years building smaller companies first. Platform Petroleum had been developing and operating its Egbaoma marginal field since the 2002/2003 licensing round. That operational track record was the credential that allowed them to participate in the much larger Shell divestment.

And that marginal field opportunity existed because of a deliberate government policy intervention. The 2002/2003 Marginal Field Bid Round created a protected entry lane for small indigenous operators. Fields that IOCs had discovered oil in but left undeveloped for ten-plus years. Confirmed discoveries with known reserves and reduced royalty rates, 2.5% for onshore fields below 5,000 bopd, versus the then-standard approximately 20% under older terms. Not exploration gambles. Starter assets.

Think about that. The government did not say “go find oil and compete with Shell.” It said: “Here are proven reserves. Reduced royalties. Simplified terms. This is your entry lane.” And then small companies used those starter assets to build track records that qualified them for bigger opportunities.

By late 2024, confirmed in 2025, indigenous companies accounted for over 50% of Nigeria’s total oil and gas output for the first time in history. Shell, ExxonMobil, Eni, TotalEnergies, all sold onshore assets to local companies. Seplat completed its $1.28 billion ExxonMobil (MPNU) acquisition.

Now compare this to what RE developers get. DARES is a $750 million World Bank initiative targeting 17.5 million Nigerians. Real and significant. But grants are paid after commissioning, not before. Developers must pre-finance everything. There is no farm-in/farm-out mechanism. Revenue depends on community willingness-to-pay. No secondary market exists for operating assets.

Africa GreenCo is the closest thing to a renewable energy equivalent of the marginal field programme, and it is already operational. GreenCo is a creditworthy intermediary offtaker and energy trader in the Southern African Power Pool. It purchases power from renewable IPPs and re-sells to utilities and commercial buyers, absorbing the offtaker credit risk that makes IPP investment impossible when the counterparty is an insolvent state utility. The US Development Finance Corporation committed a $40 million facility to GreenCo in October 2024, backing over 350 MW of renewable capacity across Zambia, South Africa, and Namibia. GreenCo explicitly addresses “structural and market weaknesses rather than just financial symptoms.”

The lesson: farm-in, do not die. A developer who originates a project has created genuine value. That value should be exchangeable: farm out 60-70% to a capital partner, retain a carried interest and the O&M contract. GreenCo proves the intermediary offtaker model works. The deal exchange for C&I solar does not yet exist.

* * *

Africa’s Own Proof of Concept: Telecom Towers and Geothermal Wells

You do not even need to look outside the continent. Africa has already built two foundry models.

Telecom towers. Mobile operators, MTN, Airtel, Glo, originally built and owned their own towers. Capital-intensive and non-core. The solution: sell to specialised towercos and lease back. IHS Towers, founded in Lagos in 2001, grew to 39,229 towers across seven operating markets by end of 2024. The model separated infrastructure ownership from service delivery. PwC found that operators that separated infrastructure assets enjoyed valuation premiums of 30% to 50%.

Yes, MTN announced a $6.2 billion deal to reacquire IHS in February 2026. The “disaggregation failed” takes flooded my timeline. They are wrong. MTN is reacquiring because it accounts for roughly 70% of IHS’s revenue. At that concentration, the independent model is economically irrational for this specific case. The reacquisition is the exit, not the failure. For renewable energy, where demand is far more fragmented, no single offtaker would ever reach 70%. The RE towerco model would have a much longer independent lifecycle.

Geothermal in Kenya. This is the parallel nobody in the solar conversation knows about, and it is the most direct proof that the foundry model works in African energy. Kenya’s Geothermal Development Company, established in 2008, absorbs the riskiest phase of geothermal development: exploration and drilling. GDC drills wells and develops steam fields. Private operators then sign agreements to purchase steam and build power plants. At the Menengai field, GDC drilled wells producing 105 MW of steam capacity. Sosian Energy’s 35 MW plant started supplying power to the grid in 2023.

GDC is the geothermal foundry. It processes the raw resource so that “fabless” IPPs can build power plants without needing to develop geothermal expertise or absorb resource risk. The CIF/AfDB Menengai case study states it directly: “The GDC model shifts exploration and resource risks away from private investors.”

This is not a future concept. It is operational. In Africa. Today. The question is why nobody has built the equivalent for solar.

The lesson: disaggregation works when the shared infrastructure layer is excellent. The RE towerco or YieldCo that buys operating projects at predictable terms does not exist in West Africa. Its absence is the single most expensive structural gap in the market.

* * *

The Countries That Built the Foundry: India, Brazil, and Morocco

The parallels above are from other industries and one African sector. But three countries have built the actual energy foundry, the shared market infrastructure for renewables, and the contrast with the rest of Africa is so stark it should end every conversation about bankability.

India. In 1987, the same year Morris Chang founded TSMC, India established IREDA. A government-owned non-banking financial institution with one job: finance renewable energy projects from conception to post-commissioning. IREDA did not just lend money. It standardised loan structures. It built technical appraisal capacity so banks did not have to evaluate solar technology from scratch on every deal. It took long-tenor risks that commercial banks refused. By FY2026, IREDA’s loan book stood at ₹93,075 crore, approximately $10 billion. Loan sanctions in FY2025 hit ₹47,453 crore, a 27% year-on-year increase.

Then India added SECI, a procurement intermediary that aggregates demand through centralised auctions and on-sells to distribution companies, providing a creditworthy central offtaker. India’s IEX energy exchange has over 8,100 participants including more than 2,100 renewable generators. The virtuous cycle: auction certainty generates financing appetite. IREDA can lend against a predictable forward project pipeline because SECI creates it.

Result: India installed 24.5 GW of solar in 2024. Nigeria installed 803 MW in 2025, its strongest year ever. A 25x difference in annual deployment. Architecture, not sunshine.

Brazil. BNDES, Brazil’s development bank, has financed roughly 70% of all renewable energy projects in Brazil since 2000, with documented financing of $33.1 billion for the 2004-2020 period. BNDES standardised project finance structures. It imposed local content requirements that drove manufacturers to build Brazilian factories. And competitive federal auctions provided revenue certainty that made ordinary bank lending sufficient.

Result: Brazil surpassed 55 GW of installed solar capacity in 2025, more than doubling in two years. Federal auction prices have cleared around $32 per MWh. Private corporate PPAs have gone even lower. Solar is now on track to overtake hydropower as Brazil’s second-largest power source by 2032.

Morocco. This is the example that eliminates the “that will not work in Africa” objection. Morocco’s MASEN, the Moroccan Agency for Sustainable Energy, functions simultaneously as procurement authority, project co-developer taking 25% equity stakes in project SPVs, financing intermediary receiving DFI loans and on-lending to project companies, and strategic policy actor. Its Noor Ouarzazate complex, 580 MW of concentrated solar and PV, was financed with $1.6 billion from seven DFIs. Morocco now has over 4,680 MW of operational renewable capacity and targets 52% renewables by 2030. MASEN has Green Climate Fund accreditation, enabling it to access GCF financing directly.

MASEN absorbs sovereign and regulatory risk for private investors. It runs transparent competitive procurement. It uses each bidding round to stimulate local manufacturing capacity. It is the most complete integrated state renewable energy development institution in Africa. And it exists. Right now.

The lesson: the foundry is a specific set of institutions. A specialised green lender that standardises loan structures. A procurement intermediary that aggregates demand. An exchange that creates price transparency. Local content policy that builds domestic supply chains. A state development agency that absorbs early-stage risk. India, Brazil, and Morocco built these. The rest of Africa has fragments of each and none at scale.

* * *

The Consumer Foundry: What M-KOPA and Sun King Built

There is one more parallel that most C&I energy people dismiss. They should not. Because it solves the same problem at a different scale.

M-KOPA solved the consumer solar bankability problem not by finding already-bankable customers but by creating bankability. An embedded GSM chip enables remote monitoring and disabling, solving the collateral problem with IoT instead of legal contracts. Daily M-Pesa payments create a credit track record that substitutes for a credit bureau.

Sun King scaled this further. In May 2023, Sun King completed a $130 million securitisation, the first of its kind in Sub-Saharan Africa for off-grid solar. Then in July 2025, Sun King closed a $156 million securitisation of approximately 1.4 million solar products, backed by five commercial banks: Absa, Citi, Co-operative Bank of Kenya, KCB, and Stanbic Bank Kenya, plus three DFIs: British International Investment, FMO, and Norfund. The largest securitisation in Sub-Saharan Africa outside South Africa. D.light has done $490 million in total securitised financing since 2020.

The progression from $130 million to $156 million in two years illustrates market maturation. Sun King and M-KOPA did not lower the cost of capital by finding better borrowers. They lowered it by building the information infrastructure that lenders require. This is the foundry in its most elegant form: shared technology infrastructure that converts un-bankable transactions into bankable ones.

CrossBoundary Energy Access is building this in mini-grids. CBEA finances construction and owns assets. The developer focuses on origination and operations. The developer retains minority equity and the O&M contract. In January 2026, CBEA completed the first acquisition of an operational mini-grid platform, ANKA in Madagascar. The mini-grid sector quietly built the foundry that C&I solar has not.

The lesson: the foundry concept applies at every market level. M-KOPA is the foundry for consumer credit. CBEA is the foundry for mini-grid capital. GDC is the foundry for geothermal risk. GreenCo is the foundry for offtake credit risk. Nobody has built the equivalent for C&I solar in West Africa.

* * *

The Architecture, Not the Finance

Let me pull all seven parallels together.

In Cleantech 1.0, the survivors built services layers and recurring revenue.

In semiconductors, TSMC separated capital-intensive manufacturing from knowledge-intensive design, and government capital underwrote the infrastructure layer.

In Nigerian oil and gas, government-created entry lanes gave indigenous companies a structural pathway that raw competition never would have.

In telecoms, tower separation unlocked capital.

In Kenyan geothermal, GDC absorbed resource risk so private operators could deploy.

In India, Brazil, and Morocco, specialised green lenders, procurement intermediaries, and standardised auctions created the rails that made deployment possible at scale.

At the consumer level, M-KOPA and Sun King built information infrastructure that manufactured bankability from un-bankable customer bases.

Every time, the intervention that worked was architectural. Every time, the intervention that failed was financial tweaking on a broken structure.

The German Energiewende did not work because German banks invented sophisticated blended finance. It worked because a 20-year feed-in tariff guarantee made ordinary bank lending sufficient. A German Sparkasse could look at 20 years of revenue certainty and extend credit to a farmer with solar panels on a barn roof. The instrument was not sophisticated. The guarantee made sophistication unnecessary. By 2012, nearly half of Germany’s installed renewable capacity was owned by citizens, farmers, cooperatives, and small businesses. There are over 350 Sparkassen in Germany.

The Rural Electrification Administration, created by executive order in 1935 and given permanent legislative mandate through the Rural Electrification Act of 1936, did not work because rural Americans got better financial products. In the mid-1930s, nine out of ten rural farms had no electricity. The response was to reorganise the market. Create rural electric cooperatives. Change the ownership model entirely. Provide 2% loans of up to 35 years to those cooperatives. Not to individual projects. To the organisations themselves. By 1953, over 90% of US farms had electricity, at roughly half the cost private utilities had estimated.

Khanna and Palepu, the Harvard economists who coined “institutional voids,” described precisely this. In emerging markets, the absence of credit bureaus, contract enforcement, quality certification, professional intermediaries, forces firms to internalise costs that markets would otherwise absorb. Each firm fills the same voids individually, at enormous cost.

The foundry fills those voids for all participants simultaneously.

Drawing from all seven parallels, the foundry performs four specific functions. Risk absorption: GDC absorbs exploration risk, GreenCo absorbs offtake credit risk, MASEN absorbs financing intermediation risk. Standardisation: SECI and Brazil’s auctions standardise procurement, enabling price discovery and capital formation. Scale aggregation: IREDA aggregates small project demand into financeable portfolios. Market signalling: Germany’s feed-in tariff provides the long-dated revenue certainty against which commercial banks can lend.

The African energy sector needs an institution, or a set of coordinated institutions, that performs all four functions. Some pieces already exist. InfraCredit provides naira-denominated credit guarantees. GreenCo intermediates offtake risk. ETAFA Nigeria, a $50 million local currency subordinated debt fund launched by GEAPP and Chapel Hill Denham, has deployed $10 million in concessional capital to catalyse $40 million in commercial finance for distributed renewable energy. Each is a partial foundry. None covers the full stack.

The question is not whether this architecture is needed. It is whether it will be built fast enough.

Part 3 covers the two-thirds of the market I was not looking at, the residential boom and the mini-grid frontier, and the specific interventions that would actually build the foundry. Plus a survival playbook for developers who need to make it through the next three to five years while the market catches up.

This is an architecture problem.

* * *

P.S. I spent three weeks reading about semiconductor fabrication plants for this piece. My brother asked me what I was working on and I said “a blog post about solar panels.” She looked at my screen, which had a 40-page McKinsey report about chip foundries open, and said “you need to go outside.” She is not wrong. But also, the fact that a 1987 Taiwanese chip factory explains why a solar developer in Lagos cannot close a deal in 2026 is either the most important insight in this series or proof that I have lost the plot entirely. I am genuinely unsure which.

P.P.S. Nigeria’s government just approved a ₦4 trillion bond to settle power sector debts and signed a ₦100 billion bank facility for mini-grid developers. The political will is not zero. What is missing is the institutional design that converts political will into market architecture. Morocco had a King who decided renewable energy was a national priority. Nigeria has a federal system where twelve states are simultaneously building their own electricity markets. Different governance. Same foundry problem. Arguably harder. Definitely more interesting.

P.P.P.S. The German Energiewende section required me to learn what a Sparkasse is. It is a German savings bank. There are over 350 of them. They funded more renewable energy than any venture capital firm in history, not because they were innovative, but because a 20-year government tariff guarantee made the lending decision boring. The most transformative energy policy in modern history worked because it made finance boring. I think about this constantly. The African energy sector is addicted to innovative finance. What it needs is boring finance backed by credible policy. Nobody will fund a conference panel on “making energy finance more boring.” Somebody should.

P.P.P.P.S. I cited Williamson, Perez, Mazzucato, Khanna, and Palepu in a blog post about solar panels. My PhD supervisor will either be proud that I am applying academic frameworks to real-world problems or concerned that I am using a Substack to avoid writing my actual thesis. Both interpretations are correct. A full reference list for all data cited across this series is available below. If you made it to the fifth P.S. section, you are either my mother or someone who genuinely cares about African energy market structure. Either way, thank you.

Kay is Manager for West Africa at Berkeley Energy Corporate Solutions, where he structures and finances renewable energy projects across 16 countries in West and Central Africa. He is a PhD researcher in multi-physics modelling of solar-biomass-hydrogen hybrid systems at the University of North Dakota, and writes The Impostor’s Guide to Clean Energy at kaykluz.com. The views expressed here are his own and do not represent the views of his employer.

References

1. Cost of Capital & Opening Frame

Clean Air Task Force (October 2024). High Capital Costs Are Stalling Clean Energy Investment Across Africa. catf.us

International Energy Agency (June 2024). Clean Energy Investment for Development in Africa. iea.blob.core.windows.net (PDF)

2. Carlota Perez Framework

Perez, Carlota (2002). Technological Revolutions and Financial Capital. Edward Elgar. e-tcs.org (PDF)

Wikipedia. Technological Revolutions and Financial Capital. en.wikipedia.org

Perez, Carlota. TRFC Chapter 4. carlotaperez.org (PDF)

3. Mazzucato Framework

Mazzucato, Mariana & Penna, Caetano. Beyond Market Failures: The Market Creating and Shaping Roles of State Investment Banks. INET Working Paper. ineteconomics.org (PDF)

Mazzucato, Mariana (2015). From Market Fixing to Market Creating. ISIGrowth Working Paper. isigrowth.eu (PDF)

4. Cleantech 1.0

Gaddy, Sivaram, Jones, Wayman (July 2016). Venture Capital and Cleantech: The Wrong Model for Clean Energy Innovation. MIT Energy Initiative MITEI-WP-2016-06. energy.mit.edu (PDF)

Van den Heuvel, Matthias & Popp, David (2022). The Role of Venture Capital and Governments in Clean Energy. NBER Working Paper 29919. nber.org (PDF)

Bessemer Venture Partners (November 2022). Eight Lessons from the First Climate Tech Boom and Bust. bvp.com

Utility Dive (2013). How Opower Sells Energy Efficiency to Utilities. utilitydive.com

MIT Sloan. First Solar Case Study. mitsloan.mit.edu (PDF)

Kunz v. SunEdison Class Action Documents. classaction.org (PDF)

Bloomberg (April 2016). SunEdison Files for Bankruptcy After Acquisition Binge. bloomberg.com

U.S. Department of Energy Inspector General. Solyndra Special Report 11-0078-I. energy.gov

Fortune (August 2015). Why the Solyndra Mistake Is Still Important to Remember. fortune.com

TechCrunch (February 2022). African Startups Raised Record-Smashing $4.3B to $5B in 2021. techcrunch.com

5. Semiconductor / TSMC Analogy

Wikipedia. Morris Chang. en.wikipedia.org

SemiWiki. How Philips Saved TSMC. semiwiki.com

Construction Physics (May 2024). How to Build a $20 Billion Semiconductor Fab. construction-physics.com

Taipei Times (March 2026). TSMC Nets Nearly 70% of 2025 Foundry Market. taipeitimes.com

The Edge Malaysia (March 2025). IDM Market Growth 2007-2024. theedgemalaysia.com

SNS Insider / GlobeNewswire (October 2024). Semiconductor Fabless Market Report 2024-2032. globenewswire.com

Naeher, Suzuki & Wiseman (Autumn 2011). The Evolution of Business Models in a Disrupted Value Chain. McKinsey on Semiconductors. mckinsey.com (PDF)

National Central University (2004). The Vertical Disintegration of Taiwan’s Semiconductor Industries. scholars.ncu.edu.tw

Asterisk Magazine (March 2026). The Institute Behind Taiwan’s Chip Dominance. asteriskmag.com

The Korea Herald (2025). Samsung Foundry and IP Leakage Concerns. koreaherald.com

Williamson, Oliver E. (2009). Nobel Prize Lecture: Transaction Cost Economics. nobelprize.org

6. Seplat / Nigerian Oil & Gas

Wikipedia. Seplat Petroleum Development Company. en.wikipedia.org

Platform Petroleum. Official History. platformpet.com

NUPRC. Guidelines for the Award and Operations of Marginal Fields in Nigeria. nuprc.gov.ng (PDF)

Mondaq. Marginal Fields and the Petroleum Industry Act 2021. mondaq.com

Morgan Lewis. Nigeria Overhauls Its Oil and Gas Laws with Petroleum Industry Act. morganlewis.com

BusinessDay Nigeria (February 2025). We Control 50% of Nigeria’s Oil Production. businessday.ng

Punch Newspapers (December 2024). Seplat Completes $1.28bn Purchase of Mobil Nigeria. punchng.com

7. Africa GreenCo

Africa GreenCo. Official website. africagreenco.com

DFC / Africa GreenCo. DFC Commits a USD 40m Facility to GreenCo. africagreenco.com (PDF)

Engineering News (October 2024). USD 40m Facility to GreenCo. engineeringnews.co.za

8. Telecom Towers / IHS

IHS Towers. Official History. ihstowers.com

IHS Towers 2024 Annual Report (Form 20-F). ihstowers.com (PDF)

IHS Towers Press Release (February 2026). IHS Towers Announces Proposed Sale to MTN Group. ihstowers.com

MarketForces Africa (February 2026). Highlights of MTN-IHS Towers $6.2bn Acquisition Deal. dmarketforces.com

PwC (October 2025). Telecom Operators: Reinventing Their Business Models. pwc.com

9. Kenya Geothermal / GDC

Wikipedia. Geothermal Development Company. en.wikipedia.org

GDC. 15 Years Milestones Blog. gdc.co.ke

CIF/GDI. Menengai Case Study Kenya. effectivecooperation.org (PDF)

ThinkGeoEnergy. 35-MW Menengai Geothermal Power Plant Starts Grid Supply. thinkgeoenergy.com

Green Building Africa (August 2023). Sosian Energy Commissions 35MW Geothermal Power Plant in Kenya. greenbuildingafrica.co.za

CIF/AfDB. Kenya Menengai Geothermal Development Project Supplementary Document. cif.org (PDF)

10. India (IREDA, SECI, IEX)

Wikipedia. Indian Renewable Energy Development Agency. en.wikipedia.org

Business Standard (April 2026). IREDA Loan Book Climbs 22% YoY in March 26. business-standard.com

Economic Times (March 2025). IREDA Reports 27% Rise in Loan Sanctions in FY25. economictimes.com

SECI. What We Do. seci.co.in

Indian Energy Exchange (IEX). iexindia.com

PV Magazine (January 2025). India Adds Record 24.5 GW of Solar in 2024. pv-magazine.com

Leadership Nigeria. Nigeria Installs 803MW of Solar Capacity in 2025. leadership.ng

11. Brazil (BNDES)

New Development Bank (2024). BNDES Project Performance Evaluation Report. ndb.int (PDF)

Energy Tracker Asia. Solar Energy in Brazil. energytracker.asia

EIA (September 2025). Brazil Solar vs Hydropower Trajectory. eia.gov

12. Morocco (MASEN)

World Bank / PPIAF. Morocco Noor Ouarzazate Solar Complex Case Study. ppp.worldbank.org (PDF)

Climate Investment Funds (February 2016). World’s Largest Concentrated Solar Plant Opened in Morocco. cif.org

Energy Partnership Morocco. MASEN News. energypartnership.ma

Green Climate Fund. MASEN Accredited Entity. greenclimate.fund

13. Nigeria — DARES

World Bank Press Release (December 2023). Nigeria to Expand Access to Clean Energy for 17.5 Million People. worldbank.org

Nigeria Energy Transition Office. DARES Programme. energytransition.gov.ng

14. M-KOPA / Sun King / Consumer Foundry

GSMA Mobile for Development. M-KOPA. gsma.com

Sun King (2023). $130 Million First-of-its-Kind Securitisation. sunking.com

Sun King (July 2025). $156M Securitisation to Deliver Solar for Over a Million Kenyans. sunking.com

Citi Press Release (July 2025). Citi Sun King Securitisation Deliver Solar Million Kenyans. citigroup.com

Kenyan Wall Street (July 2025). Sun King Secures Record-Breaking US$156 Million. kenyanwallstreet.com

D.light / PR Newswire. D.light Closes USD125M Securitization Facility. prnewswire.com

15. CrossBoundary Energy Access / Mini-Grids

CrossBoundary (January 2026). CrossBoundary Energy Access ANKA Mini-Grid Acquisition Madagascar. crossboundary.com

CrossBoundary. Energy Access Open-Sources Project Financing Approach for Mini-Grids. crossboundary.com

16. ETAFA / InfraCredit

Global Energy Alliance for People and Planet / Chapel Hill Denham. $50M Energy Transition Africa Fund Nigeria. energyalliance.org

InfraCredit Nigeria. Financial Guarantee Product. infracredit.ng

17. German Energiewende

Clean Energy Wire. Defining Features of the Renewable Energy Act (EEG). cleanenergywire.org

EnergyTransition.org (October 2013). Citizens Own Half of German Renewables. energytransition.org

EnergyTransition.org (January 2014). The Hidden Power of Local Finance. energytransition.org

Deutscher Sparkassen- und Giroverband (DSGV). dsgv.de

18. US Rural Electrification Administration

WECI. Powering Rural America: The REA of 1936. weci.net

Wikipedia. Rural Electrification Act. en.wikipedia.org

University of Wisconsin Rural Electric Research. reic.uwcc.wisc.edu

National Park Service. Rural Electrification. nps.gov

U.S. Code Title 7 Chapter 31 Subchapter III. Rural Electrification Act Statute. uscode.house.gov

Investopedia. Rural Electrification Act. investopedia.com

Richmond Fed. Economic History — Rural Electrification. richmondfed.org

19. Academic Frameworks

Khanna, Tarun & Palepu, Krishna (July 1997). Why Focused Strategies May Be Wrong for Emerging Markets. Harvard Business Review, Vol. 75(4). institutional voids paper (PDF)

Perez, Carlota (2002). Technological Revolutions and Financial Capital. PDF

Mazzucato, Mariana (2015). From Market Fixing to Market Creating. PDF

Williamson, Oliver E. (2009). Nobel Prize Lecture. nobelprize.org