The Foundry Problem (Part 1): Why African Renewable Energy Companies Keep Dying

The real problem is not bankability. It is market structure. And the Iran war just made it impossible to ignore.

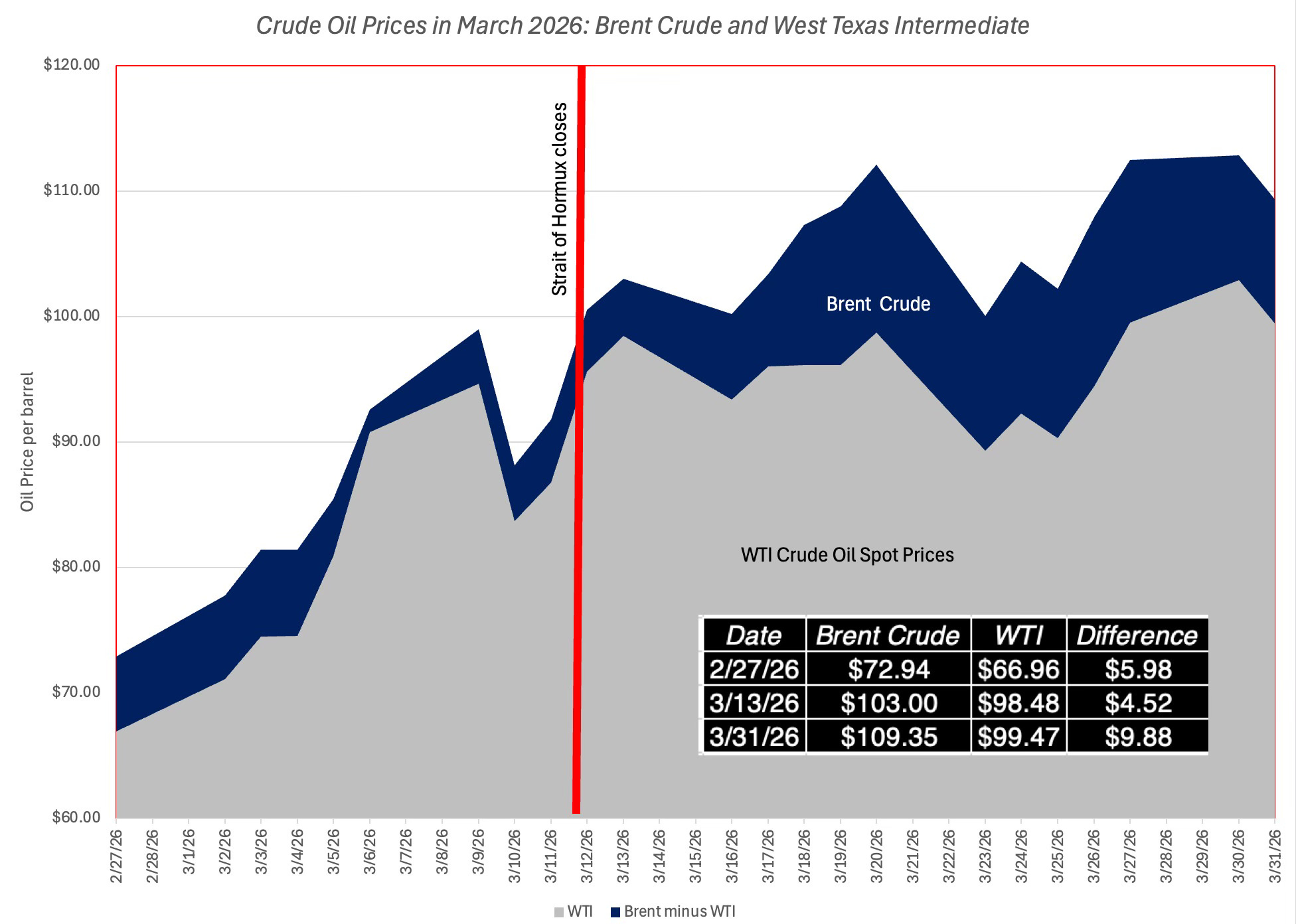

Brent crude, which traded at around $70 a barrel before the war, has surged past $110 in early April [1]. A rise of more than 50% in five weeks.

The Strait of Hormuz, the narrow passage through which roughly a quarter of the world’s seaborne oil trade flows [2], has been functionally closed since the US and Israel attacked Iran on February 28, 2026 [3]. The IEA’s Fatih Birol said it plainly: “Today, we are losing 12 million barrels per day [4], surpassing the combined losses of the 1973 and 1979 oil crises.” Qatar has declared force majeure on its LNG exports [5]. Saudi Aramco’s Ras Tanura terminal has shut down [6]. US gas prices hit $4 a gallon by the end of March [7]. Goldman Sachs has modelled a severely adverse scenario reaching $160 [8] a barrel. Wood Mackenzie and Macquarie analysts are warning of scenarios approaching $200 [9].

Africa is getting hammered.

Ghana raised petrol prices 15% [10]. Tanzania, 33% [11]. Gambia, nearly 19% [12]. Botswana, Mali, South Africa, all scrambling. The World Economic Forum noted [13] what should be obvious: poorer fuel-importing states in Africa and Asia cannot absorb these shocks the way wealthier nations can. For them, the pain arrives as higher household prices, fiscal strain, and a greater risk of rationing or unrest.

The 2026 spike is a cyclical shock. Africa’s dependence on imported fuels is structural.

And this is happening against a backdrop where the US president pulled America out of the Paris Climate Agreement for the second time in January 2026 [14], gutted the IRA’s solar and wind credits through the One Big Beautiful Bill [15], and made it clear that American climate finance for Africa is not coming. When the US steps back from Paris and hollows out the IRA, it is not symbolism. It removes one of the largest prospective anchors for concessional climate capital that African DFIs were counting on. The EU, meanwhile, is watching its own gas and oil routes destabilise and diverting money into domestic resilience: storage, interconnectors, renewables at home. Africa is last in that queue.

I am sitting in Lagos, watching diesel generators rumble to life across every industrial estate in the city, burning fuel that now costs more than it did last month, which cost more than the month before, and thinking: Africa holds roughly 40% of the world’s solar potential. How are we still this dependent on a shipping lane in the Persian Gulf?

The answer is not technology. Solar PV is the cheapest source of new electricity generation [16], on a levelised cost basis, in most African countries. It is not demand. Around 80% of Nigerian companies cite electrification challenges [17] as their most significant obstacle to doing business. It is not even money, in the aggregate. Clean energy investment on the continent reached approximately $40 billion in 2024 [18], more than double the 2019 figure, in a year when global clean energy investment hit $2 trillion.

The answer is market structure.

Whether this war lasts six months or three years is almost secondary to what it reveals about the way we have built our markets. And for 600 million Africans without grid access, the same states most exposed to fuel price spikes are also most exposed to climate impacts. That doubles the cost of delay.

Let me be precise about the problem this series is addressing. African renewable energy developers, the small and mid-sized companies that originate, develop, finance, build, and operate solar projects, mini-grids, and distributed energy systems, are dying. Not in dramatic bankruptcies. In the slow bleed of running out of working capital while waiting for projects to close. The market structure around them is broken in specific, diagnosable, fixable ways. And every other industry that faced the same structural problem eventually found the same kind of answer.

This article shows how the current architecture kills developers. Part 2 looks at industries that fixed the same problem. Part 3 sketches what we need to build now.

* * *

The Conversation That Never Changes

I have been having the same conversation for three years.

Different rooms. Different cities. Lagos, Accra, Casablanca, Abidjan, sometimes Nairobi. Different developers sitting across from me. But the shape of the conversation is always the same, almost word for word, like we are all reading from a script that nobody wrote down.

A developer has a pipeline. Three or four C&I solar projects, maybe a biomass opportunity. One of them is real: a real industrial client, a real energy load, real diesel bills eating into margins that were already thin before Hormuz closed. The developer has done a site visit. They have a relationship that took eighteen months to build.

Then the conversation stalls.

Not because the economics are bad. Diesel at $0.35/kWh against a solar PPA at $0.10 was already compelling. At $110 oil, with diesel heading north of $0.50/kWh in some markets, it is an emergency. Not because the technology is uncertain. Not because demand is absent.

The conversation stalls because the developer cannot get the project financed. And they cannot get it financed because they cannot prove bankability. And they cannot prove bankability because they have no track record. And they cannot build a track record because they cannot close their first project. Eighteen to thirty-six months from first conversation to commissioning is normal for a 1 to 5 MW C&I project. Almost no local developer is capitalised for that kind of runway.

This is the classic SME “missing middle” problem, dressed up in kilowatts and PPAs. The SME financing gap in Sub-Saharan Africa is estimated at $331 billion [19]. In African climate tech specifically, EchoVC Partners found that less than 10% of all deals fall in the $250,000 to $1 million range, the exact band where most ventures need capital to transition from proof-of-concept to commercial readiness. Across all African climate tech, just 10 companies captured more than half of all capital.

Even the IFC’s own Scaling Solar initiative, designed specifically to solve this problem with DFI backing and standardised frameworks, failed to scale in Africa [20], per a 2023 Devex investigation. If even a well-resourced IFC initiative could not build the rails, that tells you the problem is structural, not operational.

* * *

What the Rest of the Nigerian Economy Understood

Let me tell you about companies that solved a version of this problem.

In 2015, a company called TeamApt started building backend banking software for other people’s banks. Nobody noticed. It spent four years as a plumbing company, generating revenue from invisible infrastructure work. When they started, POS terminals were an afterthought product for incumbent banks. Then TeamApt pivoted. Rebranded as Moniepoint. Started deploying those terminals to market women in Lagos, Ibadan, Kano. By 2024, Moniepoint was processing over ₦412 trillion in transactions [21], handling roughly 80% of in-person payments in Nigeria [22]. TIME named it one of the world’s 100 most influential companies [23]. Valuation: over $1 billion.

Moniepoint did not start by trying to be a unicorn. It started by generating revenue from infrastructure nobody else wanted to build. It is the foundry concept in action: shared infrastructure enabling distributed operators.

A foundry is an infrastructure business that standardises high fixed-cost work, whether chips, payment rails, or refineries, so others can build on top of it.

Aliko Dangote built a nearly $20 billion refinery [24] in Ibeju-Lekki, not because Nigeria had a supportive regulatory environment for refining. Nigeria exported crude and imported refined fuel for decades. Dangote built it anyway. He vertically integrated an entire supply chain: port, pipeline, crude import deals, downstream distribution. Because the shared infrastructure for each of those functions did not exist. That is what the absence of a foundry costs at scale. No solar developer can spend $20 billion building their own institutional infrastructure.

By 2025, the Dangote Refinery was supplying 18 million litres of gasoline per day [25]. When the Iran war hit and European countries started buying aviation fuel from Lagos for the first time in history, the bet looked less like ambition and more like prophecy. The expansion to 1.4 million barrels per day, partnering with Honeywell [26], targets 2028.

Or look at Rensource. Ademola Adesina started it in 2015 as a power-as-a-service company for Nigerian market traders. When the pandemic halted that business, the team built Sabi, a B2B marketplace for informal merchants, which hit $1 billion in annualised GMV [27] and raised $66 million at a $300 million valuation. Sabi then pivoted again into traceable mineral supply chains through its TRACE platform [28], helping Africa capture more value from its critical mineral reserves. This is what a foundry-thinking company does: it builds shared infrastructure that enables an entire sector, then adapts the infrastructure as sectors evolve.

Nigeria’s top nine fintechs are worth a combined $10.6 billion [29]. Flutterwave at $3 billion. OPay at $2.75 billion. Moniepoint at $1 billion. Paystack, acquired by Stripe for more than $200 million [30], just created The Stack Group [31], a holding company with a payments unit, a microfinance bank, a consumer app, and a venture arm. In telecoms, towercos like IHS and Helios took network infrastructure off operator balance sheets so everyone could focus on customers and spectrum instead of steel and concrete. In data centres, MainOne and Rack Centre built the pipes so everyone else could sell services.

In the AI industry, OpenAI, Anthropic, Mistral, and others built foundry infrastructure first, letting the market form around it. Meta open-sourced Llama. Amazon invested $8 billion in Anthropic [32]. They were building foundries, not competing for individual chip designs.

Here is what Moniepoint, Dangote, Sabi, and OpenAI share: they built market infrastructure rather than competing within a broken market. The renewable energy sector has no equivalent. No shared rails. No common standards. No foundry. Every developer is building their own refinery from scratch, one project at a time.

This is not a technology problem. It is an architecture problem.

* * *

The Wrong Diagnosis: Bankability Versus Architecture

The dominant narrative in African energy finance is that African projects are not bankable. DFIs repeat it. Development banks repeat it. Lenders who spent thirty minutes with a project information memorandum repeat it.

It is the wrong diagnosis.

Bankability is a symptom, not the disease. The disease is a capital stack mismatch so severe that even good projects cannot find the right money at the right stage of development.

Think of the capital stack as four distinct risk buckets: idea risk, development risk, construction risk, and operating risk. In African clean energy, buckets one and four are almost empty, while three is over-subscribed.

Stage One: Origination and Pre-Development. Tens of thousands of dollars over 6 to 18 months. Patient capital that tolerates high failure rates. Almost entirely absent. DFI grants usually pay consultants and studies, not payroll. They de-risk assets for lenders but do not extend the runway for the developers creating those assets.

Stage Two: Late Development. Low hundreds of thousands over 12 to 24 months. Equity that funds legal, environmental, technical, and financial costs. Scarce and expensive. The developer gives away too much equity to access too little money.

Stage Three: Financial Close. Multi-million dollar project finance debt. Available from DFIs and commercial lenders for projects with credible offtakers. This is the capital that shows up in press releases. Traditional project finance is optimised for de-risked, late-stage assets. It was never designed to fund origination at scale in fragmented markets.

Stage Four: Company Capital. The most absent capital of all. Recurring operating lines. The entire ecosystem finances projects, not companies. But companies die between closings, not during them.

Here is the number that makes this concrete. Africa’s average weighted cost of capital for renewable energy projects is 15.6%, versus 4.2% in Western Europe [33], per the Clean Air Task Force. For Nigeria specifically, the WACC for renewable energy is 25 to 31%, per the Climate Policy Initiative [34]. An Ortelius analysis made the point viscerally: the identical solar park that costs €86/MWh to build in Europe at 5% WACC costs €135/MWh in Africa at 12% WACC [35].

The sun is the same. The technology is the same. Only the financing cost is different.

And then there is the currency mismatch. Most projects are financed in dollars or euros but generate revenue in naira, cedis, or shillings. The Energy for Growth Hub quantified it: currency mismatch alone adds 5 to 6 percentage points [36] to the effective cost of capital and pushes the LCOE for utility-scale solar in Africa to 10 to 15 cents per kilowatt-hour. Two to three times higher than in Europe or Asia. Not because the sun is weaker. Because the financial architecture is broken.

Africa’s solar installations fell from 3.07 GW in 2023 to 2.4 GW in 2024 [18], in a year when global clean energy investment hit $2 trillion. Clean energy investment on the continent reached approximately $40 billion in 2024 [18], roughly 2 to 3% of the global total, against an estimated need of $200 billion per year [37].

This is a textbook case of coordination failure: no single actor can justify investing in early-stage pipelines or shared standards, so everyone waits for someone else to move first.

* * *

Who Survives When Architecture Is Missing

Look at who actually survived in this market. And look at what they have in common.

Daystar Power is Shell [38]. Not Shell-backed. Shell. Acquired outright, operating with an oil major’s balance sheet. Offering C&I solar PPAs at half the grid price, recently announcing its expanded footprint in the Agbara industrial estate, pushing deeper into Nigeria’s manufacturing heartland.

BECS, is backed by Berkeley Energy, which manages billions of dollars renewable energy funds across Africa and Asia. Starsight recently raised $15 million in mezzanine funding from British International Investment [39] on top of its AIIM/Helios equity backing. Empower New Energy, backed by Climate Fund Managers (a Dutch-South African entity) and Norfund (Norway’s development finance institution) [40], just financed a JustRite Superstores solar installation across multiple locations. Husk Power, backed by Shell, Engie, and IFC, is raising toward an IPO targeted for 2027 [41].

Konexa is incubated by Shell Foundation, Rockefeller Foundation, DFID, and USAID [42], with MIGA guarantees. UBA recently did a solar deal with Renewvia.

The common denominator is not technology or execution. It is access to cheap, patient, foreign balance sheets that reprice risk and smooth volatility. In practice, this means control over African power assets is quietly migrating to balance sheets in London, Oslo, New York, and The Hague, even when the assets sit in Lagos or Accra. A local developer raising naira-denominated working capital at mid-teens effective interest rates simply cannot match Shell’s dollar cost of capital on a 15-year PPA.

But the market is not closed. Daystar’s own feasibility analysis identified 170,000 C&I businesses [43] in Nigeria as potential solar customers. They serve a few thousand. Less than 2% penetration. You know who else left 98% of their addressable market untouched? The big Nigerian banks. For decades, First Bank, UBA, and GTBank served maybe 30 million Nigerians. Then OPay, Moniepoint, and PalmPay raced to sign up the other 170 million.

The renewable energy version of this play: projects below 2 MW, regional manufacturers in tier-two cities, biomass CHP, industrial process heat, hybrid systems. A developer who understands the energy profile of a cassava processing plant is competing on knowledge, not cost of capital. The foreign-backed platforms are not even looking for those deals.

This is not a technology problem. It is an architecture problem.

* * *

The Iran Factor, Trump, and Three Triggers

The Iran war does three things to this picture simultaneously.

First, it makes the economic case for solar undeniable at the C&I level. Jeff Currie, Chief Strategy Officer [44] of Energy Pathways at Carlyle and a former Goldman Sachs energy analyst with a 25-year track record, said at CERAWeek: “We are going to get the energy transition forced on us in a very painful way.”

Subsidy removal in May 2023 flipped the economics for households. Grid collapses in 2024 forced SMEs to scramble. The Iran war hits C&I balance sheets directly. Three triggers, three customer segments.

Second, it exposes the structural absurdity of Africa’s energy position. Nigeria is a crude oil exporter and a refined fuel importer. Dangote Refinery is now bailing out European airlines with aviation fuel from Lagos. But Nigeria cannot deploy solar at scale on its own factory roofs. The country with the refinery that European airlines are scrambling to buy fuel from cannot figure out how to finance a 2 MW solar installation in Ibadan.

Third, and this is the part the clean energy community has not processed yet: the US is not coming to help. Trump has made that explicit. The EU is diverting capital into domestic resilience before thinking about Africa. Every assumption about where the money for African energy transition was supposed to come from is being rewritten. Yet the Iran war also creates a window: DFIs and European governments are now prioritising energy resilience as a geopolitical imperative. African distributed solar is not just a development play anymore. It is strategic infrastructure. That reframing changes who the investors are.

* * *

The Solar Import Trap and the Manufacturing Gap

Nigeria imported ₦435.52 billion worth of solar panels [45] in 2025, with 71.38% from China [46]. REA’s managing director, Abba Aliyu, put a number on the problem: over ₦200 billion spent annually importing PV panels. “We want to reverse that trend,” he said.

This is energy’s version of the old commodity trap: export raw materials, import finished goods, and let currency swings determine who survives. We are replacing dependence on Gulf oil with dependence on Chinese manufacturing.

In October 2025, the Minister of Power, Adebayo Adelabu, hosted the inaugural Nigerian Renewable Energy Innovation Forum at the Transcorp Hilton, themed “Implementing the Nigeria First Policy.” Vice President Shettima opened it. Nearly $500 million [47] in announced or committed investment deals were signed for solar panel assembly, battery manufacturing, and local component production. Adelabu declared that Nigeria is on track for nearly 4 GW per annum of solar manufacturing capacity [47]. By October, Nigeria had begun exporting locally manufactured solar panels to Ghana [48].

Then Adelabu resigned to contest the Oyo State governorship election. The minister who was championing local manufacturing is now running for governor. The policy momentum he created has yet to find its next champion.

The Dufil Group, makers of Indomie noodles, understood something about local manufacturing that the solar industry has not figured out. When Dufil entered Nigeria, it built factories. It localised production. Flour Mills of Nigeria followed the same playbook. Dangote followed it in cement, sugar, refining. The solar industry has no equivalent. No local panel assembly at meaningful scale. Every project is a dollar-denominated import transaction in a naira economy. The naira went from approximately ₦460 to the dollar in early 2023 to ₦1,535 by end-2024 [49], a collapse in dollar purchasing power of more than 70%. Every solar panel got proportionally more expensive.

If a Tier-1 platform is landing panels at 18 to 20 cents per watt and a small developer pays 23 to 25 cents, your project-level LCOE gap is locked in before you design anything.

For comparison: India installed 24 GW of solar in 2024 alone. Nigeria installed 803 MW in 2025 [50], its strongest year ever, and was celebrated as Africa’s second-largest market. The gap is not resource or ambition. It is architecture: India has IREDA, SECI, standardised auctions. Nigeria does not.

* * *

The EV Boom’s Connection to Solar

While the energy sector argues about bankability, another transition is happening on Nigerian roads.

Between 15,000 and 20,000 electric vehicles [51] now drive in Nigeria. SAGLEV has a dedicated EV assembly plant [52] in Imota, Lagos, scalable to 10,000 units per year. Spiro has deployed over 60,000 electric motorbikes [53] with more than 1,200 battery swap stations across Africa. Foltï Technologies launched eDryv in Lagos [54], Nigeria’s first ride-hailing platform powered by solar-charged EVs. Ecowaka, led by Prince Ojeabulu [55], is manufacturing electric keke napeps starting at ₦2.6 million. The Federal Executive Council approved ₦58 billion in December 2025 for 200 electric buses [56]. Nigeria signed a deal with South Korea for an EV manufacturing plant [57] targeting 300,000 vehicles annually.

My brother, mentor, and former colleague John Okoro, co-founder and Managing Director of Growth Energy (part of the Solio Group, headquartered in France), recently commissioned the largest solar-powered EV charging station in East Africa [58], in Burundi. Growth Energy operates across Nigeria, Burundi, Tanzania, Zanzibar, and Kenya. John’s work demonstrates something profound: the EV-solar convergence is not a future possibility. It is being built right now.

Every EV is a mobile battery. In a grid with chronic outages, that is not just a transport asset. It is potential backup storage. For a solar developer, EV charging is exactly the kind of predictable, high-load, daytime-skewed demand profile that makes mini-grids and C&I systems bankable. Yet EV and power regulators rarely talk. There is no standard tariff, no integrated planning, almost no concessional capital for solar-powered charging corridors.

The EV boom and the solar boom are the same transition, being discussed in separate conference rooms by separate industries with separate investors. That is the architecture problem in miniature.

* * *

The Ecosystem That Is Actually Forming

This is what a proto-foundry looks like: not one big company, but many specialised firms standardising messy bits of the value chain.

On February 23, 2026, the Rural Electrification Agency signed an MoU with Lotus Bank unlocking a ₦100 billion revolving credit facility [59] for mini-grid developers participating in the DARES programme. Up to ₦8 billion per developer. 18-month tenor tailored to the real construction cycle of sub-5 MW projects. A Nigerian bank providing project-level lending at the ticket sizes developers actually need. That is architecture changing.

Sterling Bank secured a $13 million facility from the Universal Green Energy Access Programme [60], managed by Cygnum Capital, to expand renewable energy lending in Nigeria. Viathan, Nigeria’s leading embedded energy company, launched Decentralised Energy Limited with $10 million in equity from the Anergi Group [61] and ₦8.5 billion in debt, backed by an investor community that has committed over $100 million to Viathan over the past decade. DEL is an attempt to turn one company’s investor relationships into a platform. A mini-foundry.

Rivy, a climate finance platform, has disbursed over ₦43 billion and approved 38,000 loans [62]. Then Rivy registered solar mini-grids for International Renewable Energy Certificates, increasing the supply of RECs from solar assets in Nigeria by 25% within a month. I-RECs turn each MWh of clean electricity into a tradable certificate. That extra revenue can raise project IRRs by 1 to 3 percentage points on small systems. Solad Integrated Power, running solar mini-grids at Iponri market in Lagos, sold its first I-RECs through Rivy’s platform, with backing from SEforALL. Carbon finance making mini-grid economics work.

SunFi, founded by Rotimi Thomas, has deployed over 1,500 solar systems managing over 4 MW [63] of assets, connecting Nigerians to solar through financing plans. Uwana Energy is connecting households to solar loans. Fixr, at usefixr.com, is building the installation and maintenance services layer.

InfraCredit Nigeria announced a credit guarantee for Africa’s first solar panel assembly plant [64], combining local currency instruments with Bank of Industry concessional capital. This attracted Nigerian pension funds and insurance companies: domestic institutional capital that previously could not participate in energy infrastructure. That is landmark. Not because of the deal size, but because it proves that local currency guarantees can unlock domestic institutional capital for renewable energy manufacturing.

The IFC and AfDB launched Zafiri in October 2025 [65], a dedicated equity vehicle for distributed energy companies, specifically addressing the missing middle. Their own framing: a “missing middle” problem requiring “long-term equity to these providers.” The Africa Mini-Grid Developers Association, under its new leadership, continues the coalition-building work that individual developers cannot: standardising documentation, aggregating policy advocacy.

A taxonomy of what is forming: financing rails (Rivy, SunFi, Uwana, Lotus Bank), services rails (Fixr, installers), policy rails (AMDA, REA), risk-mitigation rails (I-RECs, carbon finance, InfraCredit guarantees). The pieces exist. The integrated system does not.

* * *

Three Regulatory Shifts That Change the Terrain

NBET becomes NENEX. The Federal Government approved NBET’s transition to an energy commodity exchange modelled on India’s IEX [66], which cleared over 100 billion kWh in FY2024 with more than 8,100 participants [67] including over 2,100 renewable generators. In practice, a 1 to 10 MW solar plant near an industrial cluster can list on the exchange and sell to multiple buyers instead of begging one anchor offtaker for a 15-year PPA.

The Electricity Act 2023 devolution. Twelve Nigerian states have enacted their own electricity acts, with three fully taking charge. LASERC has assumed full regulatory authority [68] in Lagos. This decentralisation is a double-edged sword: more regulators can mean more market access, but also more fragmentation. Regulatory resets are painful, but they are also rare windows where nimble players can grab licences and shape rules. President Tinubu signed the Electricity Act Amendment 2025 in February 2026 [69], further clarifying state powers.

DARES at scale. Nigeria’s $750 million Distributed Access through Renewable Energy Scale-up [70] programme, targeting 17.5 million Nigerians through solar mini-grids and standalone systems, is part of Mission 300, the World Bank/AfDB joint programme to connect 300 million Africans to electricity by 2030. The first DARES disbursements were enabled by the Lotus Bank MoU. That MoU is already performing foundry functions.

Regulation is quietly shifting from vertically-integrated monopolies to market-platform logic. Developers who think like infrastructure-as-a-service providers will win.

* * *

The Question

So here is what I keep coming back to.

Nigeria has fintech companies worth a combined $10.6 billion [29]. It has the Dangote Refinery expanding to become among the largest on earth, exporting refined fuel during a Middle Eastern war. It has 20,000 EVs on its roads and a local assembly plant. It has solar panel exports to Ghana and carbon finance platforms registering I-RECs from market mini-grids.

And yet. The renewable energy sector, in a country where the sun beats down 300 days a year, cannot reliably finance a 2 MW rooftop installation.

The foundry problem is that we have developers and demand, but no shared infrastructure that turns bespoke projects into repeatable products.

What would the foundry be? Standardised PPA templates that any developer can use without commissioning bespoke legal work. A credit database that converts a developer’s five-year operational track record into a bankable risk profile. A local-currency refinancing vehicle that allows a developer who built a project on expensive dollar debt to refinance in naira once the asset is proven. A technical standards body whose sign-off is credible to international lenders without each developer hiring their own international advisory team.

This is not new. This exact dynamic has played out in semiconductors, Cleantech 1.0, Nigerian oil and gas, and telecoms. Every time, the industry eventually found a structural answer.

Part 2 of this series opens those history books. We will ask what an African TSMC for power might look like: a platform that standardises contracts, capital, and components so developers can specialise in origination and operations.

The war in the Gulf will not last forever. Oil prices will stabilise. But the structural vulnerability, the fact that the continent with the most solar potential on earth is still dependent on a shipping lane 8,000 kilometres away, will persist until somebody builds the infrastructure that makes it unnecessary.

The foundry problem is not about money. It is about architecture.

And the clock is ticking.

* * *

P.S. And no, I am not entirely sure that writing a blog post about solar financing that includes electric tricycles, the Strait of Hormuz, Indomie noodles, and OpenAI in the same argument is evidence of coherent thinking. But the connections are real. The structural parallels are real. And if drawing the lines between them makes even one small developer rethink their approach on Monday morning, then these were worth it.

* * *

Kay is Manager for West Africa at Berkeley Energy Corporate Solutions, where he structures and finances renewable energy projects across 16 countries in West and Central Africa. He is a PhD researcher in multi-physics modelling of solar-biomass-hydrogen hybrid systems at the University of North Dakota, and writes The Impostor’s Guide to Clean Energy at kaykluz.com. The views expressed here are his own and do not represent the views of his employer.

* * *

References

[1] Fortune, Oil Price Tracker, April 3, 2026. https://fortune.com/article/price-of-oil-04-03-2026/

[2] U.S. Energy Information Administration, Strait of Hormuz. https://www.eia.gov/todayinenergy/detail.php?id=65504

[3] Britannica, 2026 Iran War. https://www.britannica.com/event/2026-Iran-war

[4] CNBC, IEA’s Fatih Birol, April 1, 2026. https://www.cnbc.com/2026/04/01/oil-price-iea-fatih-birol-brent-iran-strait-hormuz.html

[5] Reuters, QatarEnergy Force Majeure, March 4, 2026. https://www.reuters.com/business/energy/qatarenergy-declares-force-majeure-lng-shipments-2026-03-04/

[6] Reuters, Saudi Aramco Ras Tanura, March 2, 2026. https://www.reuters.com/business/energy/saudi-aramco-shuts-ras-tanura-refinery-after-drone-strike-source-says-2026-03-02/

[7] CNN, US Gas Prices Hit $4, March 31, 2026. https://www.cnn.com/2026/03/31/business/us-gas-prices-usd4-intl

[8] Fox Business, Goldman Sachs Oil Scenarios, March 2026. https://www.foxbusiness.com/economy/iran-war-could-push-inflation-higher-year-goldman-sachs-says

[9] Al Jazeera, Could Oil Hit $200?, March 19, 2026. https://www.aljazeera.com/news/2026/3/19/could-oil-hit-200-a-barrel-analysts-no-longer-think-its-far-fetched

[10] GhanaWeb, Fuel Price Increase, April 2026. https://www.ghanaweb.com/GhanaHomePage/business/Petrol-diesel-prices-to-rise-by-15-from-April-2026-Benjamin-Nsiah-2026861

[11] The Chanzo, Tanzania Fuel Prices, April 1, 2026. https://thechanzo.com/2026/04/01/tanzanias-fuel-prices-surge-to-record-highs-as-middle-east-war-drives-global-oil-crisis/

[12] The Point, Gambia Fuel Prices, April 2026. https://thepoint.gm/africa/gambia/headlines/fuel-pump-prices-increase-in-gambia

[13] World Economic Forum, Global Price Tag of War, March 2026. https://www.weforum.org/stories/2026/03/the-global-price-tag-of-war-in-the-middle-east/

[14] New York Times, US Exits Paris Agreement, January 27, 2026. https://www.nytimes.com/2026/01/27/climate/paris-climate-agreement-withdrawal.html

[15] PV Tech, Renewable Energy Credits in One Big Beautiful Bill. https://www.pv-tech.org/us-renewable-energy-credits-face-steep-cliff-edge-in-one-big-beautiful-bill/

[16] PV Tech / IRENA, Renewable Power Generation Costs 2024. https://www.pv-tech.org/irena-global-solar-pv-lcoe-increases-by-0-6-in-2024-to-us0-043-kwh/

[17] World Bank Enterprise Surveys, Nigeria 2025. https://www.worldbank.org/en/programs/enterprise-surveys

[18] Global Solar Council, Africa Market Outlook 2025–2028. https://www.globalsolarcouncil.org/news/global-solar-council-africas-solar-market-set-to-surge-42-in-2025-but-finance-bottlenecks-threaten-growth/

[19] MIT Sloan, Financing Africa’s Missing Middle, November 2024. https://mitsloan.mit.edu/centers-initiatives/ksc/responsibly-financing-africas-missing-middle

[20] Devex, Why a Major IFC Solar Initiative Failed, May 2023. https://www.devex.com/news/why-a-major-ifc-solar-initiative-failed-to-scale-in-africa-105513

[21] BusinessDay Nigeria, Moniepoint 2025 Year in Review. https://businessday.ng/technology/article/breaking-as-banks-pull-back-moniepoints-n1trn-loans-fill-nigerias-sme-credit-gap/

[22] TechCrier, Moniepoint 80% In-Person Payments, January 2026. https://www.techcrier.com/2026/01/moniepoint-processes-80-percent-of.html

[23] TIME, TIME100 Most Influential Companies 2025. https://time.com/collections/time100-companies-2025/7289615/moniepoint/

[24] Wikipedia, Dangote Refinery. https://en.wikipedia.org/wiki/Dangote_refinery

[25] Premium Times, Dangote Refinery Output, December 2025. https://www.premiumtimesng.com/news/top-news/841988-dangote-refinery-supplied-23-5-million-litres-of-petrol-daily-in-november-nmdpra.html

[26] Honeywell, Dangote Expansion Partnership, November 2025. https://www.honeywell.com/us/en/press/2025/11/honeywell-to-help-dangote-double-production-capabilities-at-africa-s-largest-refinery

[27] TechCrunch, Sabi $300M Valuation, May 2023. https://techcrunch.com/2023/05/19/african-b2b-e-commerce-startup-sabi-tops-300m-valuation-in-new-funding/

[28] Condia, Sabi TRACE Platform Pivot, October 2025. https://thecondia.com/sabi-minerals-pivot-trace-platform/

[29] Nigeria Communications Week, Fintech Valuations, January 2026. https://www.nigeriacommunicationsweek.com.ng/nigerias-9-top-fintech-firms-valued-at-10-6bn-in-january-2026/

[30] TechCrunch, Stripe Acquires Paystack, October 2020. https://techcrunch.com/2020/10/15/stripe-acquires-nigerias-paystack-for-200m-to-expand-into-the-african-continent/

[31] FF News, Paystack Launches The Stack Group, January 2026. https://ffnews.com/newsarticle/paytech/paystack-launches-holding-company-the-stack-group-tsg/

[32] Amazon, Investment in Anthropic, November 2024. https://www.aboutamazon.com/news/aws/amazon-invests-additional-4-billion-anthropic-ai

[33] Clean Air Task Force, WACC in African Power Sector, 2024. https://www.catf.us/resource/evaluating-weighted-average-cost-capital-wacc-power-sector-african-countries/

[34] Climate Policy Initiative, Cost of Capital for Renewable Energy, 2023. https://www.climatepolicyinitiative.org/wp-content/uploads/2023/06/Discussion-Paper-EM-Cost-of-Capital-for-RE-and-GCGF-FINAL-Jun-2023.pdf

[35] Ortelius, Cost of Capital Hits Developing Countries Hardest. https://ortelius.be/cost-of-capital-hits-developing-countries-the-hardest-in-their-green-transition/

[36] Energy for Growth Hub, Local Currency Advantages, June 2025. https://energyforgrowth.org/article/the-quantifiable-advantages-of-local-currency-on-african-energy-projects/

[37] Global Solar Council, Africa Market Outlook for Solar PV 2025–2028. https://www.globalsolarcouncil.org/resources/africa-market-outlook-for-solar-pv-2025-2028/

[38] Shell, Daystar Power Acquisition, December 2022. https://www.shell.com/what-we-do/renewable-power/renewable-power-news-releases/shell-completes-acquisition-of-solar-solutions-provider-daystar-power-group.html

[39] Africa Newsroom, Starsight / BII $15M, March 2026. https://www.africa-newsroom.com/press/starsight-energy-africa-group-starsight-partners-with-british-international-investment-bii-to-advance-clean-energy-growth-in-west-africa-through-us15-million-mezzanine-funding

[40] Empower New Energy, CFM/Norfund Partnership, December 2022. https://www.empowernewenergy.com/post/empower-new-energy-partners-with-climate-fund-managers-and-norfund-to-accelerate-solar-investments

[41] Yahoo Finance, Husk Power IPO Plans, January 2025. https://finance.yahoo.com/news/husk-power-targets-400m-funding-121530024.html

[42] Shell Foundation, Konexa, December 2019. https://shellfoundation.org/news/can-an-integrated-energy-distribution-model-turn-around-africas-ailing-utilities/

[43] Daystar Power / RMI, Feasibility Study, March 2024. https://daystar-power.com/en/news-article?post_id=176354

[44] AOL Finance / S&P Global, CERAWeek, March 2026. https://www.aol.com/finance/shift-oil-isnt-just-being-120741898.html

[45] Punch Newspapers, Solar Panel Imports, March 2026. https://punchng.com/solar-panel-imports-hit-2-9m-amid-outages/

[46] PVKnowhow, Nigeria Solar Panel Imports, October 2025. https://www.pvknowhow.com/news/nigeria-solar-panel-imports-impressive-n242-68-billion-in-2025/

[47] The Electricity Hub, Nigeria $500M Solar Manufacturing, October 2025. https://theelectricityhub.com/nigeria-secures-500m-for-solar-manufacturing-plants/

[48] Guardian Nigeria, Solar Panel Exports to Ghana, October 2025. https://guardian.ng/energy/nigeria-now-exporting-solar-panels-to-ghana-says-adelabu/

[49] Nairametrics, Exchange Rate 2024. https://nairametrics.com/2024/12/31/exchange-rate-ends-2024-at-n1535-1-marking-a-40-9-depreciation/

[50] PV Tech / Global Solar Council, Africa Record Solar Capacity 2025. https://www.pv-tech.org/gsc-africa-adds-record-4-5gw-new-solar-pv-capacity-2025/

[51] Climate Scorecard, Nigeria EVs, March 2025. https://www.climatescorecard.org/2025/03/nigeria-has-pledged-to-achieve-100-zero-emission-sales-for-new-cars-and-vans-by-2040/

[52] SAGLEV, EV Assembly Plant, May 2025. https://saglev.com/saglev-targets-10000-electric-vehicles-annual-output/

[53] TechCrunch, Spiro $100M Raise, October 2025. https://techcrunch.com/2025/10/21/spiro-raises-100m-the-largest-ever-investment-in-africas-e-mobility/

[54] TechCabal, eDryv Solar EV Ride-Hailing, April 2025. https://techcabal.com/2025/04/07/edryv-nigerias-first-95-green-powered-ev-ride-hailing-service-unveils-in-lagos/

[55] Ecowaka, Electric Keke Launch, July 2025. https://ecowaka.io/ecowaka-launches-three-wheeled-electric-vehicles-to-boost-transportation-in-nigeria/

[56] Guardian Nigeria, FEC Electric Buses, December 2025. https://guardian.ng/news/fec-endorses-new-industrial-policy-okays-electric-buses-boi-hq-others/

[57] Business Insider Africa, Nigeria–South Korea EV Deal, February 2026. https://africa.businessinsider.com/local/markets/nigeria-signs-deal-with-south-korea-to-launch-africas-first-electric-vehicle-factory/xe79vqe

[58] Growth Energy, Burundi EV Charging Station, January 2026. https://growth-energy.fr/building-africas-largest-solar-powered-ev-charging-station-in-burundi-growth-energy-gem/

[59] The Nation, REA–Lotus Bank ₦100B Deal, February 2026. https://thenationonlineng.net/rea-bank-strike-n100b-energy-deal/

[60] Cygnum Capital, UGEAP / Sterling Bank $13M, March 2026. https://www.cygnumcapital.com/news/ugeap-provides-usd-13-million-facility-to-sterling-bank-to-promote-renewable-energy-lending-in-nigeria

[61] BusinessDay, Viathan / DEL Launch, March 2026. https://businessday.ng/companies/article/decentralised-energy-secures-10m-initial-equity-funding-from-anergi-group-to-kick-start-operations/

[62] TechCabal, Rivy Carbon Finance Platform, October 2025. https://techcabal.com/2025/10/13/rivy-is-growing-the-carbon-market-in-nigeria/

[63] The Realistic Optimist, SunFi Profile, May 2025. https://www.realisticoptimist.io/sunfi-managed-solar-marketplace-in-nigeria/

[64] Energy Capital Power, InfraCredit Solar Manufacturing Guarantee, March 2026. https://energycapitalpower.com/infracredit-to-issue-africas-first-solar-panel-manufacturing-guarantee/

[65] IFC, Zafiri Launch, October 2025. https://pressroom.ifc.org/all/pages/PressDetail.aspx?ID=27872

[66] ThisDay Live, NBET Energy Exchange, March 2024. https://www.thisdaylive.com/2024/03/04/like-india-nbet-begins-process-of-transmuting-to-energy-exchange-to-revamp-nigerias-electricity-market/

[67] Indian Energy Exchange, Official Website.

https://www.iexindia.com

[68] Templars Law, LASERC Regulatory Authority, July 2025. https://www.templars-law.com/knowledge-centre/new-lagos-electricity-order-what-it-means-for-current-operators-and-potential-investors/

[69] Daily Intel, Electricity Act Amendment, February 2026. https://www.dailyintelnewspaper.com/beyond-the-grid-what-the-new-electricity-act-really-changes/

[70] Solar Quarter, Nigeria DARES Programme, March 2026. https://solarquarter.com/2026/03/20/nigerias-dares-project-to-deliver-clean-power-to-17-5-million-people-with-world-bank-support/