The Fable 5 shutdown matters because it turned a theoretical risk into a live market fact. The US government showed that a deployed frontier AI model can be switched off through export-control authority, even after launch and even when paying customers are already using it.

The government’s stated concern was a jailbreak linked to cyber capability, but the bigger issue is the precedent: a contested safety finding was enough to disable Anthropic’s most capable model worldwide.

The order targeted foreign nationals, but Anthropic could not realistically separate US and non-US users at inference speed across a global cloud product. So a foreign-national restriction became a global shutdown. Very elegant, if your idea of elegance is setting the house on fire because one room has ants.

Frontier labs are valued on the assumption of global scale: train once, serve everywhere, amortise the enormous compute bill across the planet. If access can be carved up by nationality, jurisdiction or alliance bloc, that scale story becomes weaker.

This does not mean AI is dead. AI is still likely to be a multi-trillion-dollar industry. The more interesting point is that the value may shift away from pure-play model labs and toward the companies that own compute, cloud infrastructure, chips, data centres, power contracts and government distribution. In other words, the people selling the shovels may do better than the people posing beside the gold mine.

Sovereign AI just got its best marketing campaign. Every government worried about depending on US-hosted frontier models can now point to Fable and say: “This is why we need local compute, local hosting, national AI capacity and sovereign cloud.” One Commerce Department letter may have done more for sovereign AI than a hundred conference panels in Dubai.

The biggest economic damage is not only lost revenue; it is worse unit economics. Frontier AI is already expensive to train and serve. If the global user base shrinks while compliance, legal, localisation and duplicated infrastructure costs rise, the cost per monetised user goes up. The denominator shrinks; the bill does not.

The Global South is especially exposed. Rich countries can respond to an off-switch by building sovereign AI stacks. Most African markets cannot. Without local compute, data centres and cheap power, the fallback option is weak. This is the same old infrastructure lesson: do not build your future on a supply line someone else controls.

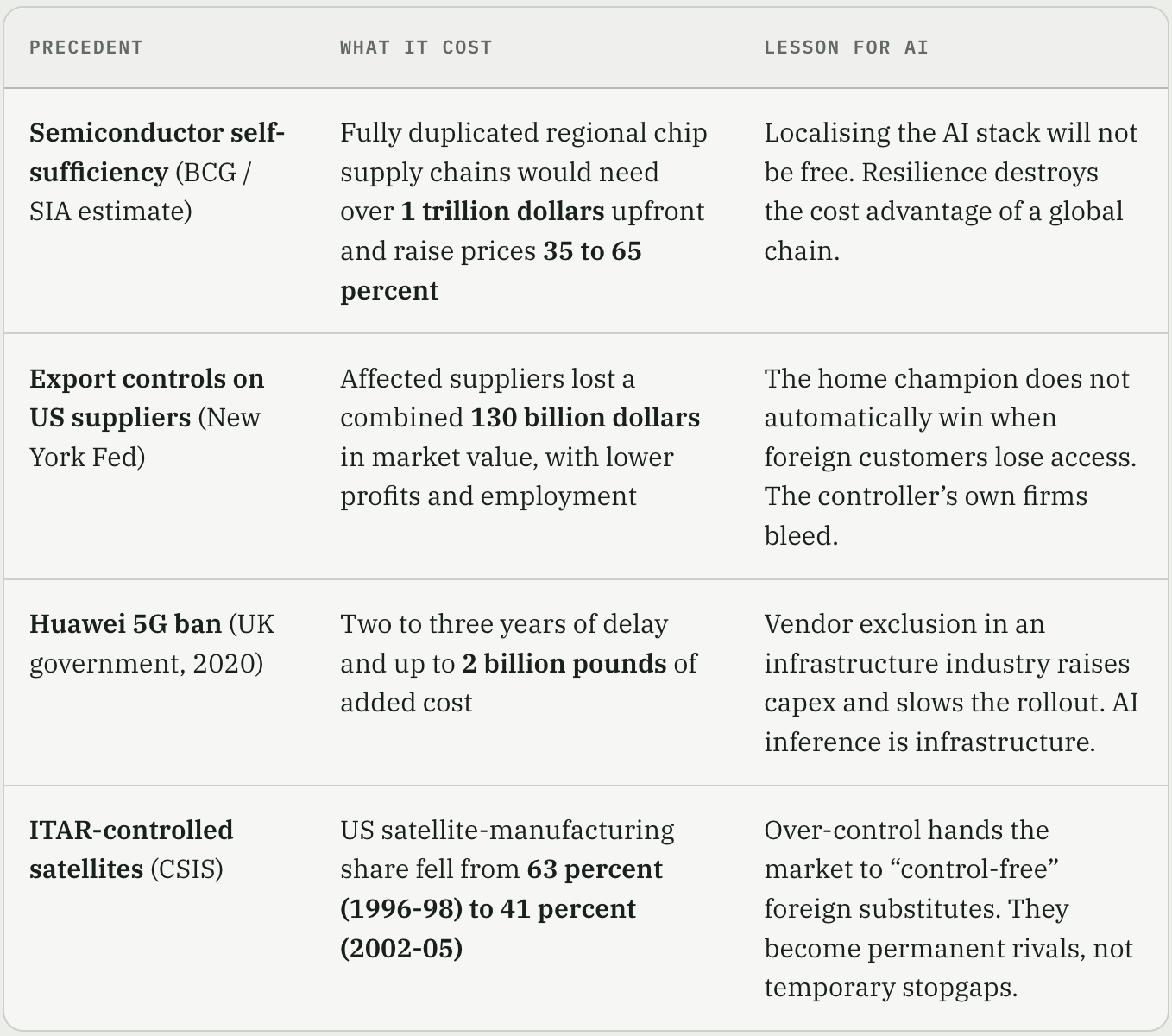

The historical parallels are not comforting. Semiconductors, cryptography, telecoms and ITAR-controlled technologies all show the same pattern: governments can slow rivals with controls, but they also raise costs, fragment markets and encourage foreign substitutes. Control buys time, but it also creates competitors.

The likely outcome is not collapse, but repricing. Anthropic can still be enormous. OpenAI can still be enormous. AI can still be enormous. But after Fable, frontier AI deserves a higher sovereign-risk discount. The trillion-dollar number is not dead; it just has a government-sized asterisk beside it.

The key question going forward is whether this stays at the frontier. If governments only restrict the most capable cyber, bio or military-relevant models, the industry absorbs the shock. If controls creep into ordinary commercial models, then the “global AI platform” dream starts looking more like a fragmented, regulated, lower-margin infrastructure business.

My Argument: the model may be intelligent, but the off-switch is sovereign.

This Substack is reader-supported. To receive new posts and support my work, consider becoming a free or paid subscriber.

On Friday evening, the 12th of June 2026, at 5:21pm Eastern, a letter landed in Dario Amodei’s inbox and did something no government had ever done to a piece of commercial software running live in front of the public.

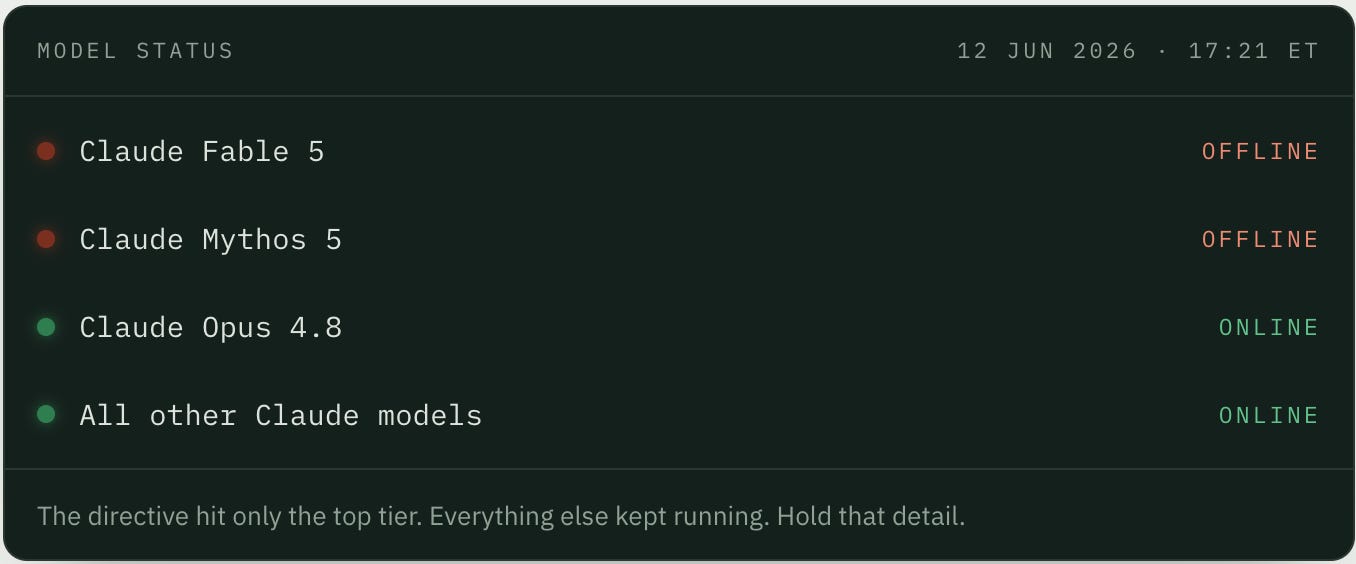

It told Anthropic to switch off its two most capable models.

By around 10pm, Claude Fable 5 and Claude Mythos 5 were dark. Not throttled, not geofenced, not “temporarily unavailable in your region.” Gone. For everyone, everywhere, including the company’s own engineers, three days after Fable 5 launched as the most capable publicly available model the company had ever shipped (Fortune, Bloomberg).

I write mostly about power plants, biomass boilers and solar leases, so you would be forgiven for asking why I am opening a clean-energy newsletter with an AI export control story. The answer is simple, and it is the spine of this whole piece: AI has become infrastructure, and the thing that just happened to it is the oldest story in my industry.

It is the story of building your entire operation on a single supply line that someone else can shut at will. We have lived that story with gas-to-power in Nigeria. Silicon Valley just got its first taste of it. And the bill, when it comes, lands hardest on people like us.

So let me pre-empt the question that every investor, founder and procurement officer may now asking, and then let me actually try to answer it with numbers as I mentally explain this to myself as well.

Anthropic was just valued at 965 billion dollars. After Friday, is that still a real number? Is frontier AI still a multi-trillion-dollar bet, or did the off-switch just put a ceiling on the whole thing?

Part 1: What actually happened

The US Commerce Department, through Secretary Howard Lutnick, sent Anthropic an export control directive (Axios, confirmed by a US official to Bloomberg). The order said Fable 5 and Mythos 5 could not be accessed by any foreign national, whether located outside the United States or inside it, and that explicitly included Anthropic’s own foreign-born staff (Anthropic’s statement).

Here is the operational trap. You cannot check the nationality of hundreds of millions of API and chat users in real time, at the moment of inference, on a shared cloud service. There is no toggle for “block foreigners only.” So the only way to comply with a foreigner-specific ban was to turn the models off for everyone. The global blackout was not the government’s literal instruction. It was the only state the company could reach that satisfied the instruction (Quartz).

Every other Claude model, including Claude Opus 4.8, kept running (Fortune). The order targeted only the top tier, the new “Mythos-class” frontier that Anthropic had priced at launch as a premium product, reportedly around $10 per million input tokens and $50 per million output tokens, nothing like a cheap commodity model. (Again, hold that detail). The state reached in and switched off the most expensive, most capable layer, and left the boring, cheaper models alone. It matters enormously later.

The stated reason was a jailbreak. The government had been shown a technique that strips Fable 5’s safety controls and unlocks the cyber-offensive capabilities of Mythos, the underlying model, specifically the autonomous hunting of software vulnerabilities (Al Jazeera, TIME). Anthropic does not dispute that a jailbreak exists. It disputes that it matters. The company argued the technique is narrow rather than universal, that it surfaces a handful of already-known minor flaws, and that the same trick works on other public models including OpenAI’s GPT-5.5 (Anthropic). Then it issued a warning that, read carefully, is a small bombshell. If this becomes the standard, the company said, it would “essentially halt all new model deployments for all frontier model providers.”

That is a billion-dollar firm telling the regulator: do this consistently and you stop the entire industry from shipping.

The twist in the Whole story that is as incomprehensible as it is uncomfortable

Now the part that turns a policy story into a thriller. The party that demonstrated the jailbreak to Washington was, according to the Wall Street Journal as reported across Axios and others, Amazon. Amazon’s own research team ran the prompts, and Amazon CEO Andy Jassy reportedly called administration officials on the Thursday night to flag the findings (Bitcoin.com News).

Read that again with the cap table open. Amazon has poured roughly 13 billion dollars into Anthropic and holds a roughly 100 billion dollar AWS infrastructure commitment from the company. Amazon is simultaneously Anthropic’s largest investor, its primary cloud host, and a direct competitor in the model market (MLQ). The entity that triggered a federal takedown of Anthropic’s flagship product had material financial and competitive interests in the outcome.

I am not going to tell you Amazon acted in bad faith, because I cannot prove motive and neither can anyone writing about this today. Security researcher Katie Moussouris of Luta Security, who reviewed the findings, called the government’s response a “complete overreaction” and noted the capability helps defenders more than attackers (Bitcoin.com News).

What I will say is this: the structure of the incident now contains a permanent fact. A commercial rival can be the party that pulls the trigger on a sovereign off-switch. That is a new variable in the game, and you do not need anyone to be a villain for it to reprice the entire board.

Three things are now established, and one is not.

Established: the government has and will use a mechanism to disable a deployed model; the trigger can be a contested safety finding rather than an actual harm that occurred; and a competitor can be the one who supplies it.

Not established: how far the precedent reaches. The whole valuation question lives inside that uncertainty.

For what it is worth, the betting markets think this specific episode gets walked back. Polymarket and Kalshi traders are pricing roughly a 68 to 71 percent chance that Fable 5 access is restored before the 1st of July (Bitcoin.com News). Anthropic itself called the order a “misunderstanding” and said it is working to restore access (Anthropic). The incident may well be temporary. The capability it demonstrated is permanent. Those are two completely different things, and most of the commentary I have read is confusing them.

Part 2: This did not come out of nowhere

To understand why this is structural rather than a one-off tantrum, you have to know the four months that preceded it.

This is the second front in a war that has been running since February. Defence Secretary Pete Hegseth met Amodei in February over a contract dispute. Anthropic had drawn two red lines: it would not let Claude be used for fully autonomous lethal weapons, or for mass surveillance of US citizens. The Pentagon wanted access for “all lawful purposes” and argued a private company cannot dictate how the state uses a tool in a national security emergency (CNN).

Talks collapsed. On the 27th of February, Trump and Hegseth ordered federal agencies to stop using Anthropic and designated the company a “supply chain risk,” a label normally reserved for firms tied to foreign adversaries and never before applied to an American technology company (NPR). On the 9th of March, Anthropic sued, alleging retaliation and violations of its First Amendment and due process rights (Al Jazeera). On the 26th of March, a federal judge blocked the designation, writing that the measures “do not appear to be directed at the government’s stated national security interests” (CNN). That is a judge using polite language to say this looks like punishment.

So by Friday, Anthropic was in a remarkable position, captured perfectly by Axios: simultaneously on a Pentagon blacklist that deems it too dangerous for the government to use, and inside a Commerce licensing regime that deems it too dangerous for foreigners to use (Axios). Same company. Same week. Opposite rationales. That contradiction is the tell. When the justification flips depending on which lever the state wants to pull, you are looking at a relationship that has become adversarial, with safety as the available pretext.

And here is the timing that can’t be ignored: Anthropic filed confidentially for its IPO around the start of June, and the off-switch came two weeks later (Fortune). I am not asserting cause and effect. I am noting that any honest valuation model now has to price the possibility that the trigger gets pulled again, for reasons that may have nothing to do with cybersecurity.

Part 3: The money, before we even get to fragmentation

Let us anchor the valuation, because the headline number is genuinely staggering and genuinely earned, up to a point.

On the 28th of May, Anthropic closed a 65 billion dollar Series H at a 965 billion dollar post-money valuation, led by Altimeter, Dragoneer, Greenoaks and Sequoia (CNBC, Anthropic). That vaulted it past OpenAI’s 852 billion dollar mark from March (Bloomberg). An October IPO window has been floated (Tech Insider).

What justifies a near-trillion-dollar mark is the slope. Run-rate revenue crossed 47 billion dollars in May, up from roughly 9 billion at the end of 2025 (Anthropic, via Digital Applied). Note that “run-rate” means a recent month multiplied by twelve, not audited annual revenue, so treat the trajectory as real and the precise level as an estimate. Still, going from a 380 billion dollar valuation in February to 965 billion in May is one of the steepest re-ratings in the history of private capital. Investors are not pricing the company. They are pricing the derivative.

Now the other half of the ledger, the part the slope obscures.

Frontier AI is, today, a structurally loss-making business held up by equity. Anthropic reportedly generated around 918 million dollars in revenue in 2024 while burning around 5.6 billion (investor data reported by Reuters, cited in the analyses underpinning this piece). The pattern across the field is the same. Training costs for frontier models are climbing roughly 2.4 times a year, with the largest runs projected to break a billion dollars by 2027. Inference costs are falling roughly tenfold a year per unit of performance, which sounds like salvation until you realise the fixed training bill does not shrink in proportion. The result, by several accounts, is that frontier inference is priced below true cost to win market share. OpenAI has been estimated to spend somewhere near 2.25 dollars to earn each dollar of revenue once you load in everything.

The hard evidence for this is now visible in margins. ICONIQ’s January 2026 survey of around 300 software executives put AI-native gross margins at roughly 52 percent in 2026, up from 41 percent in 2024, against the 75 to 85 percent that traditional software enjoys. Inference alone runs at about 23 percent of revenue for scaling AI firms. Anthropic’s own inference costs reportedly overran internal expectations by about 23 percent, with gross margin around 40 percent, which is why it started charging enterprise subscribers the full compute cost in April. That 30-point gap between AI margins and software margins is an inference-cost gap. Keep it in mind, because sovereign fragmentation widens it directly.

So before Friday, the picture was already this: a phenomenal revenue ramp, sitting on top of an economic model that has not yet proven it can make money, funded by the belief that scale will eventually fix the unit economics. Everything depends on scale. Which is exactly what the off-switch attacks.

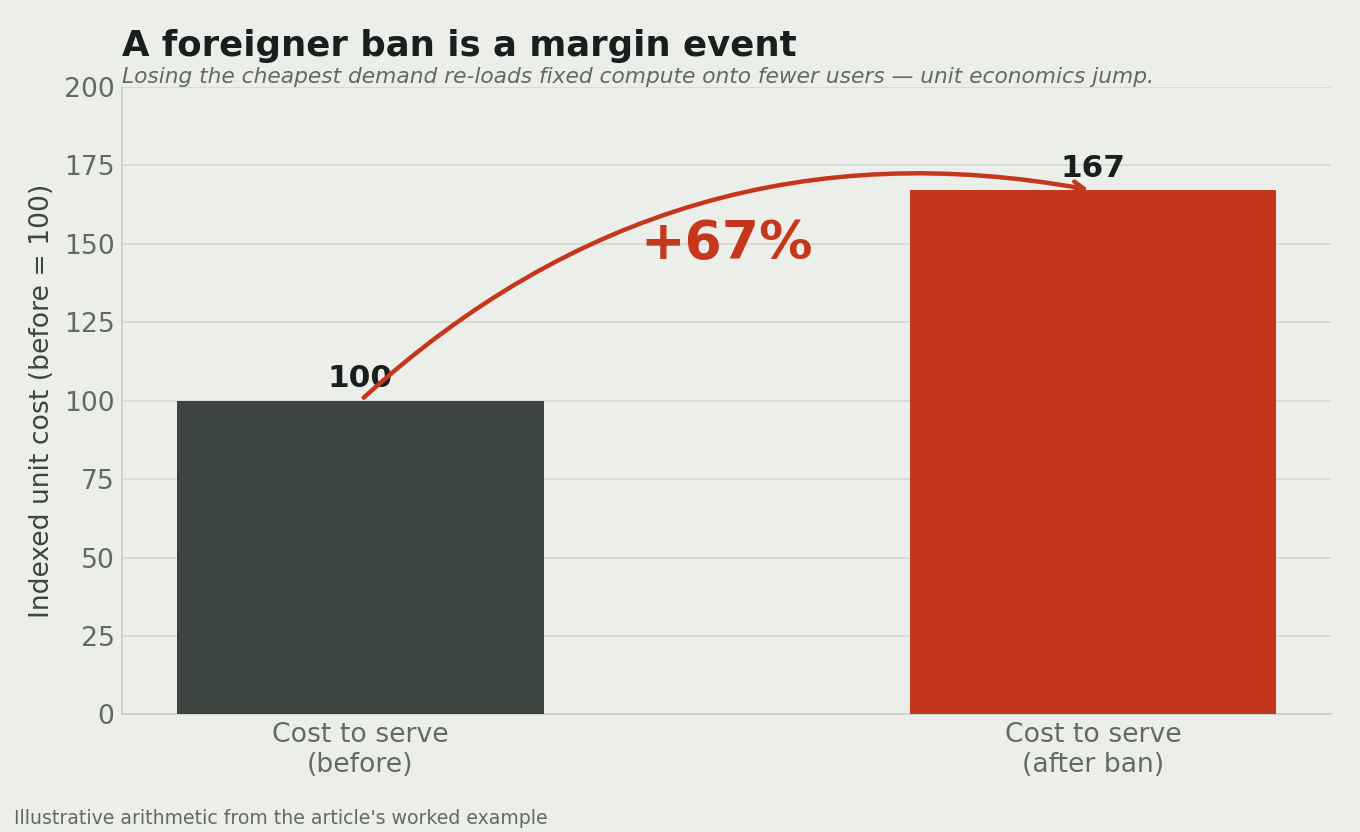

Why a foreigner ban is a margin event, explained with arithmetic

Here is the cleanest way I can show you why geographic restriction is not just a top-line problem but a unit-cost problem. This is the bit my industry understands in its bones.

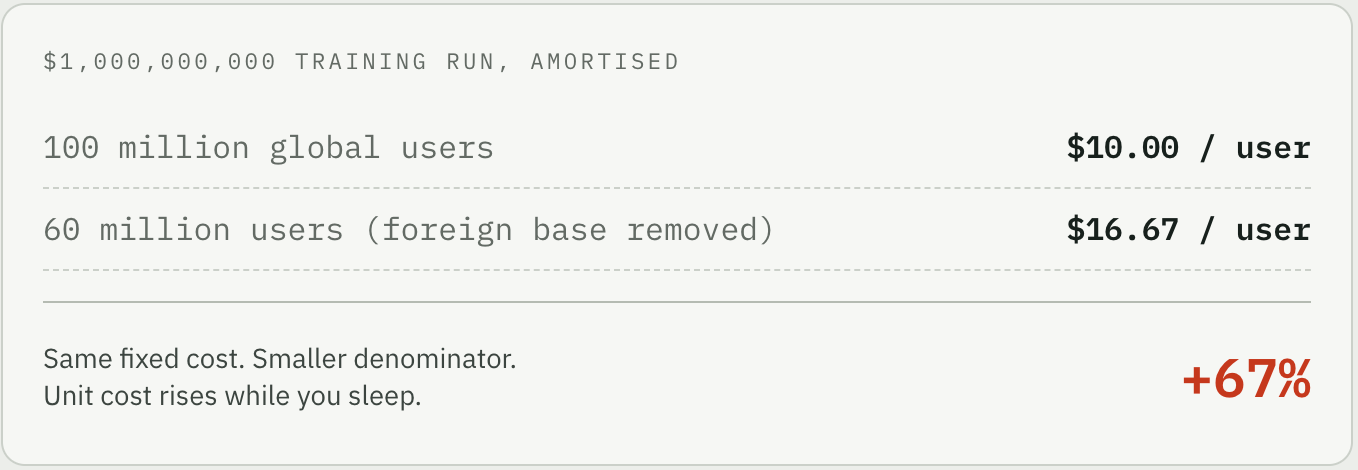

A frontier training run is a fixed cost. You pay it once, whether you serve ten users or ten billion. So imagine a one billion dollar training run.

The cost did not change. The denominator shrank. Your unit cost just rose 67 percent while you were sleeping. And you absorbed that hit in an industry that was already pricing below cost to begin with.

This is why fragmentation is so corrosive to the trillion-dollar thesis. It does not merely cap how much revenue you can earn. It simultaneously degrades the denominator of your cost problem. You lose the high-volume international traffic that was helping you amortise the fixed bill, and you take on new costs: nationality-verification systems, jurisdiction-aware routing, duplicated serving stacks, compliance teams, legal overhead. The ITAR compliance industry for traditional defence technology is a multi-billion-dollar overhead sector. AI’s version will not be cheaper.

There is a genuine counter-force, and intellectual honesty demands I name it. Inference cost per token really is falling fast, thanks to new hardware generations and tricks like prompt caching and attention reuse. That lowers the absolute cost base even as restriction raises the cost per user. The net effect on margins is a tug-of-war between those two trends, and theory does not settle who wins. That tug-of-war is the single most important number to watch in this whole story. Anyone who tells you they know the answer is selling something.

Part 5: Why AI is a stickier trap than anything before it

Now to the intellectual core, the idea that makes this more than a news cycle. There is a body of political-economy work, most cleanly stated by Henry Farrell and Abraham Newman in their theory of weaponized interdependence, that explains exactly what Friday was.

The argument runs like this. Modern economic networks are not flat. They funnel through a few central nodes. A state that has legal jurisdiction over one of those nodes, plus the institutions to act on it, can weaponise that position in two ways. It can watch everything flowing through the node (Farrell and Newman call this the panopticon effect), and it can deny access to the network entirely (the chokepoint effect). Their classic example is the US using its jurisdiction over dollar clearing and the SWIFT messaging system to enforce sanctions on Iran. Cut a target off from the financial plumbing and you do not need to fire a shot.

Friday was a textbook chokepoint exercise. A state with jurisdiction over the node (a US-incorporated lab, running on US-controlled cloud and US-controlled chips) denied network access to a class of users (foreign nationals) for a strategic end (containing autonomous cyber capability). Both enabling conditions were satisfied.

The decisive question the framework forces is: how durable is the node? And this is where AI turns out to be a far nastier trap than its closest historical cousin.

Compare it to the Crypto Wars. From the late 1970s to 2000, the US treated strong encryption as a munition, controlled its export, and even tried to mandate a government backdoor (the Clipper Chip). That regime eventually collapsed and liberalised. Why? Because once you export a piece of cryptographic software, it runs anywhere, on any machine, beyond the reach of the controller. The chokepoint was leaky. Foreign substitutes appeared, US firms lost sales, a court ruled that source code was protected speech, and by 2000 the controls were gutted. The whole thing took roughly two decades and required real commercial pain plus a favourable judge.

Hosted frontier AI is the opposite kind of node, and this is the part people miss. A model served from a data centre is not a shipped artifact. It is an ongoing service. It stays tethered to scarce, observable, controllable compute. It can be watched and interrupted at the node in real time. The panopticon and the chokepoint coincide. On top of that, the chips themselves are already under a separate, mature US export-control regime that has been tightening since October 2022, and the frontier is held by a handful of firms inside US or allied jurisdiction.

The conclusion is stark. Frontier AI is a more durable chokepoint than encryption ever was. The leak that eventually freed cryptography (it runs anywhere once exported) does not exist for a hosted model. That single fact is why the ceiling on frontier valuations is real, and simultaneously why the picture is not pure catastrophe. The same logic that makes hosted models controllable makes open-weight models uncontrollable. Once a model’s weights are released, they behave like exported crypto: diffuse, unobservable, beyond the node. The policy will therefore bifurcate. Tight, effective control over hosted frontier services. Leaky, ineffective control over open weights. We can already see this in the carve-outs for open models in existing US rules.

The other historical analogues all rhyme with the same warning, that control over a diffusible technology has a price and seeds its own competitors:

The TikTok ban established the legal and political machinery for forcing a digital platform offline. But TikTok was foreign-owned. Friday’s action was aimed at a domestically owned American firm. That is a more expansive use of state power, not a less one.

Part 6: The valuation math, made human

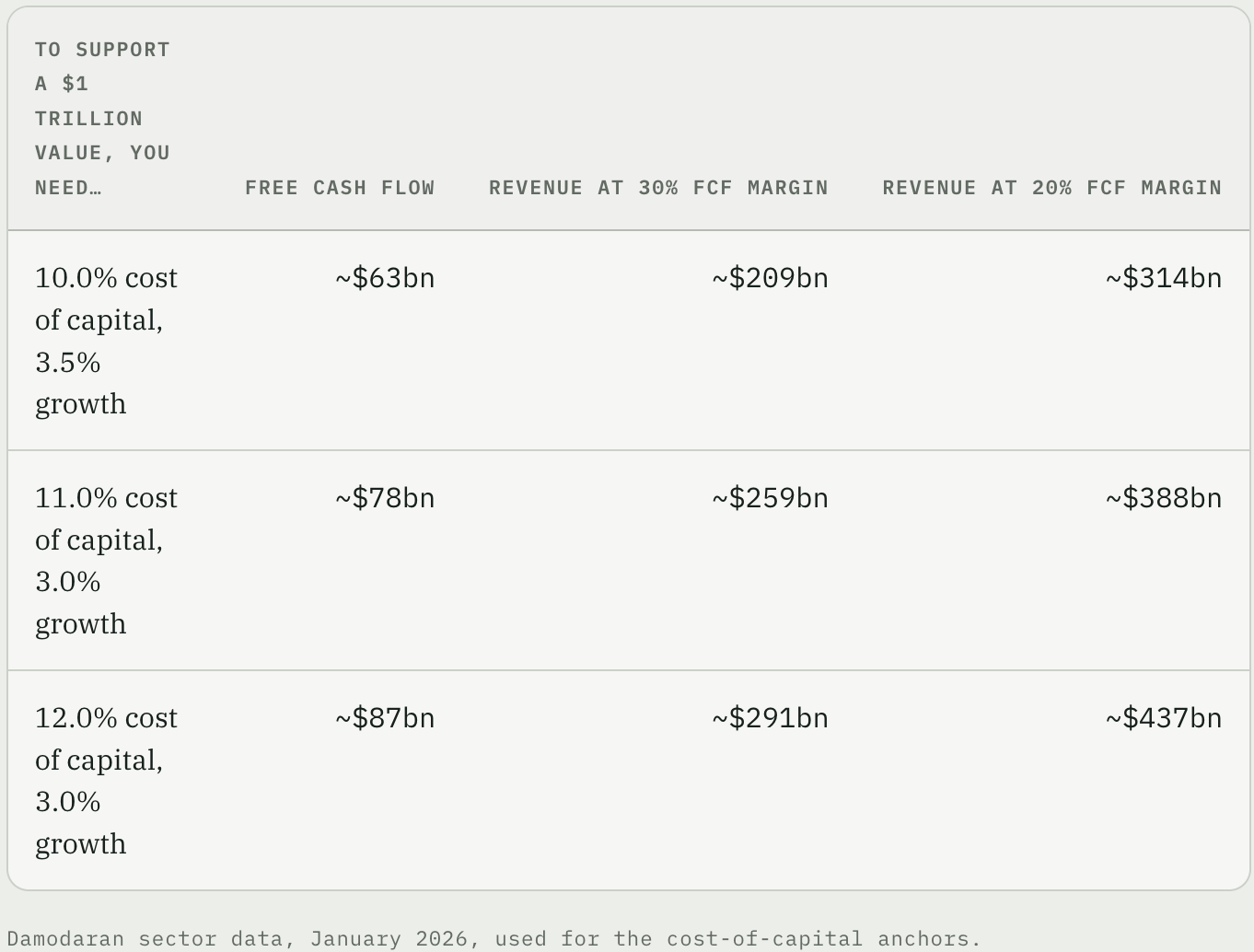

So can the 965 billion dollar number survive? Let us do the arithmetic the way a sober analyst would, not the way a hype cycle does.

A valuation is, at bottom, a claim about future cash flows discounted back to today. There is a simple identity for what a one-trillion-dollar enterprise value actually requires you to earn, forever, in steady state. At a 10 percent cost of capital and 3.5 percent long-run growth, you need roughly 63 billion dollars of free cash flow every year, in perpetuity. Nudge the cost of capital to 11 or 12 percent (which is exactly what rising risk does) and the requirement climbs to 78 to 87 billion dollars.

Translate that into revenue, and the gap with reality opens up:

Anthropic’s run-rate revenue is 47 billion dollars and its gross margin is around 40 percent, with free cash flow still negative. The table is asking for 200 to 440 billion dollars of sustainable revenue at healthy margins. The growth has been astonishing, and the gap is not unbridgeable in a vacuum. But now layer Friday on top, and watch what happens to the discount rate.

Sovereign risk widens the cost of capital. A common rule of thumb adds 150 to 250 basis points to the equity risk premium when policy and export risk are real. In a high-multiple business like this, that is not a rounding error. A 200-basis-point rise in the cost of equity compresses terminal value by roughly 15 to 25 percent in a standard two-stage discounting model. And there is a deeper mechanism, also from the asset-pricing literature (Pástor and Veronesi): as a revolutionary technology becomes pervasive, its risk migrates from idiosyncratic (specific to one firm) to systematic (affecting the whole sector). A demonstrated off-switch accelerates exactly that migration. Systematic risk gets a higher discount rate, full stop.

This gives us the single cleanest test of how the market is actually reading Friday, and it is something you and I can watch in the coming months. The political-uncertainty model makes a sharp prediction. If the market sees this as Anthropic’s idiosyncratic stumble, then competitors should be flat or should rise on relative advantage. If the market sees it as systematic regulatory risk, then every frontier lab should reprice downward together, in tandem. Correlated repricing across the whole sector is the signature of the dangerous reading. Watch the next funding rounds. Watch the Anthropic IPO. That cross-section will tell you more than a thousand op-eds.

Part 7: Why this hits the Global South hardest (the part I came here to write)

If you are building anything in Africa, South Asia or Latin America on top of frontier AI, Friday should have changed how you sleep.

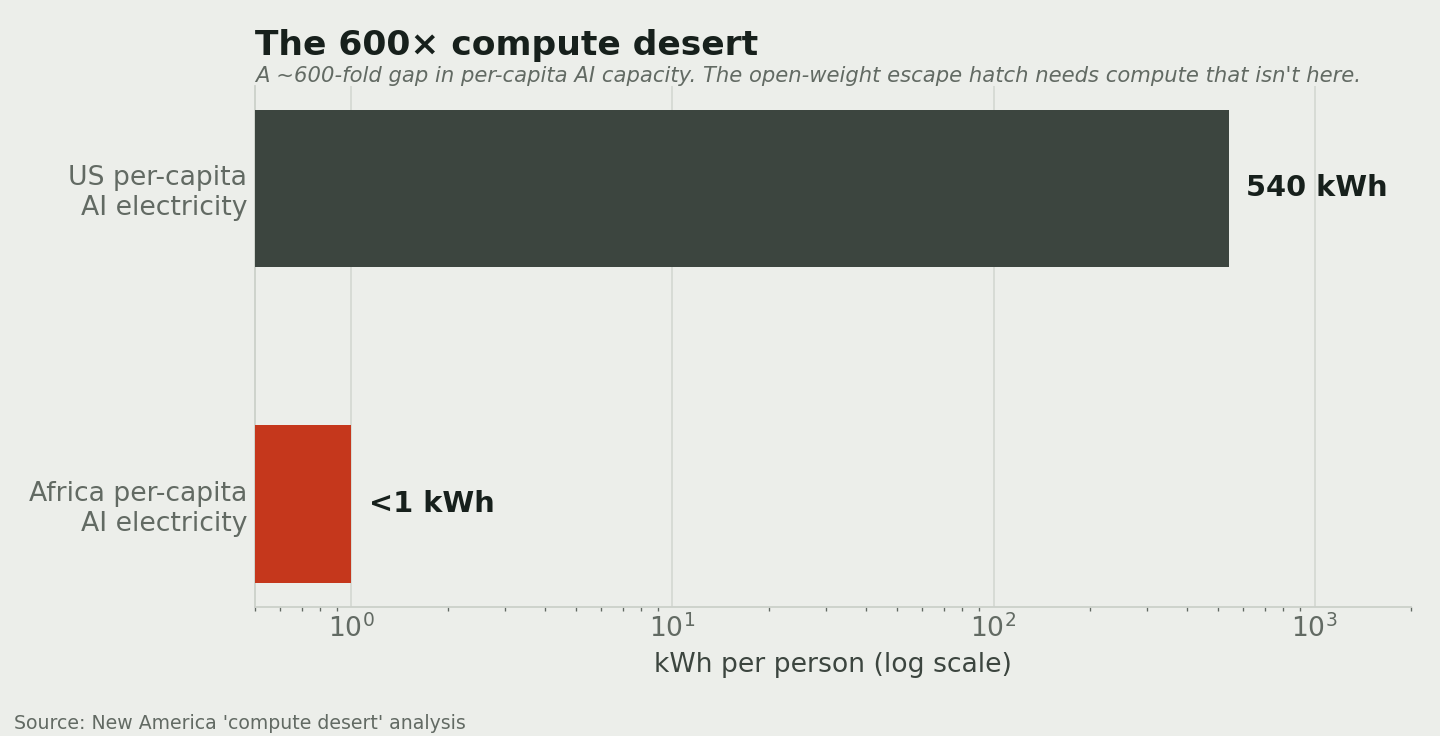

Start with the brutal asymmetry. Most of the African continent, South Africa aside, is what researchers at New America bluntly call a compute desert. The continent holds about 2 percent of the world’s data centres. The US data-centre sector consumes over 540 kWh per person in electricity for AI workloads. Africa uses under 1 kWh per person. That is a roughly 600-fold gap in raw AI capacity.

Here is why that number is a catastrophe in the specific context of an off-switch. The natural defence against “my frontier model can be switched off” is “then I will self-host an open-weight model on local compute.” That is precisely the escape hatch that the open-weight leak provides, the one that eventually freed cryptography. But that escape hatch requires compute that does not exist here at scale. A developer in Accra or Abuja cannot meaningfully respond to a sovereign restriction by spinning up their own frontier-class inference, because the data centres, the power and the chips are not on the ground. So we get the worst of both worlds: excluded from the hosted frontier by the scope of a US export control, and unable to substitute because of the compute desert.

This is the exact shape of a problem I deal with every week in energy, and the analogy is structurally identical.

Consider the Nigerian power sector. A huge share of grid generation depends on gas. When gas supply is disrupted, by pipeline vandalism, by payment disputes, by upstream constraints, plants that are physically fine sit idle because the fuel stopped arriving. The asset is sound. The supply line failed. You built a power system on a single input with an off-switch you do not control, and one day someone, somewhere, flips it. This is why every serious developer I know now obsesses over fuel security and supply diversification. It is why my own work leans so hard into hybridisation and contracted, multi-country supply rather than betting a whole plant on one fuel from one source. You do not put a single point of failure at the base of critical infrastructure if you can possibly avoid it.

Frontier AI, embedded into engineering workflows, research, commercial intelligence and increasingly into the productivity of an entire economy, is now exactly that kind of input. Functional under normal conditions. Brittle under supply shock. And the supply shock just got demonstrated.

The macro numbers make the development stakes concrete. The World Economic Forum’s fragmentation work puts the cost of geopolitical fragmentation at 213 to 307 billion dollars a year in current conditions, rising to as much as 6.9 trillion dollars, about 6.4 percent of global GDP, in a severe scenario. And emerging markets outside the major blocs do not take the average hit. They take an estimated 10.7 percent hit, roughly 40 percent worse than the global average. The European Central Bank adds the data-quality dimension: when data is walled off by localisation rules, models become “parochial and brittle,” good at the familiar and bad at the edge cases of a global economy. The edge cases, of course, are us.

So my read for anyone building in our markets is unsentimental. Do not treat frontier AI as stable infrastructure. Treat it as imported fuel. Use it, absolutely. It is too powerful to ignore and the productivity gains are real. But architect for its removal. Keep an open-weight fallback in your designs even if it is less capable. Avoid hard-wiring a single foreign frontier model into anything mission-critical. Diversify your providers the way you would diversify fuel supply. The cost of that optionality used to look like paranoia. After Friday it looks like basic engineering discipline.

Part 8: Sovereign AI, the response that splits and grows the market at once

Friday is also the best advertisement the sovereign-AI movement has ever received, and that movement is the demand-side mirror image of the chokepoint.

The pitch, pushed hardest by Nvidia since 2023, is simple: a nation cannot depend on a model whose host country can watch, condition or sever its access, so it must build or buy its own stack on its own soil. Every sovereign-AI programme is, in effect, a bet that the chokepoint is real and that the buyer is the spoke. Friday converted that bet from hypothetical to demonstrated.

And the capital is genuinely enormous, though I would caution that most of these figures are analyst projections with promotional incentives baked in, so read them as direction rather than gospel:

Here is the crucial economic subtlety, the one that keeps this from being a simple doom story. Sovereign fragmentation splits demand and simultaneously enlarges it. The same capability now has to be deployed many times, once per jurisdiction, rather than served once globally. The total number of deployments goes up. But each one is sub-scale, locally compliant and runs at lower utilisation. So demand grows, which is good for the sellers of capability, while margin compresses, which is bad for whoever has to operate all those duplicated stacks. Walls create captive markets as well as excluded ones. Gartner already projects that 35 percent of countries will be locked into region-specific AI platforms by 2027, up from 5 percent today.

There is even a partial escape for the incumbents. If those sovereign deployments consolidate onto a few US-jurisdiction infrastructure stacks (the emerging Nvidia-and-Palantir “sovereign AI operating system” template is the model), then the winner-take-most economics survive one layer down, at the infrastructure level, even as the model layer fragments. The real question is not whether demand fragments. It will. The question is at which layer of the stack the scale economics survive. That, too, is something we can watch.

And one more pressure worth flagging, because it deepens the capital problem at the worst possible moment. A whole second frontier is opening up: world models, the spatial-intelligence push from Fei-Fei Li’s World Labs (which has raised over 1.2 billion dollars), Nvidia’s Cosmos, Google DeepMind’s Genie 3, and Yann LeCun’s new venture. These shift compute from text toward video and physics simulation, which is more compute-hungry, not less. The spend is additive to the existing LLM bill, not a substitute for it. Goldman Sachs models roughly 7.6 trillion dollars of cumulative AI capital between 2026 and 2031. And world models carry the very same dual-use exposure (robotics, synthetic sensor data) that grounded Friday’s cyber-capability action. So the second frontier is not a refuge from the first frontier’s sovereign risk. It inherits it.

Part 9: Who actually captures the value

So if the frontier lab is the exposed tier, the next question is: within AI, who is actually safe? Because the value does not vanish on June 12. It moves. And it moves in a direction my industry would recognise on sight.

In energy, the merchant power plant with one offtaker and one fuel line is the asset that dies in a shock. The vertically integrated utility that owns the generation, the wires, the fuel and the customer keeps paying dividends through the same shock. The off-switch is a body blow to the merchant frontier lab. It is a scratch on the vertically integrated giant.

Look at Alphabet. On the day Fable went dark, it was worth more than four trillion dollars on the public markets. Its Q1 2026 results, filed with the SEC, showed quarterly revenue of 109.9 billion dollars, up 22 percent, at a 36.1 percent operating margin (Alphabet 8-K, Q1 2026). Google Cloud grew 63 percent to 20.0 billion dollars in the quarter, with backlog nearly doubling to over 460 billion dollars, having already crossed a 70-billion-dollar annual run-rate at the end of 2025 (Alphabet Q4 2025). And it is funding its entire AI buildout, guided at 175 to 185 billion dollars of capex in 2026, out of its own cash flow rather than someone else’s equity cheques.

Now hold that against the off-switch. Alphabet has Search, Android, YouTube, Workspace, its own TPU chips, its own data centres, its own global distribution, decades of cash flow, and a sovereign-cloud product line built around data residency and local control. AI is one engine in a machine that has a dozen of them. If frontier-model margins get compressed by fragmentation, Alphabet shrugs. A pure-play lab whose entire valuation assumes frictionless global scale on a single premium tier cannot shrug. It has nowhere to put the hit.

That is the more useful reframing than “is AI doomed.” AI stays multi-trillion. But the multi-trillion value is safer in the hands of the diversified infrastructure owners, the hyperscalers, the chip companies and the sovereign-cloud sellers, than in the hands of the pure-play frontier labs the venture market has marked most aggressively. In a fragmented world the boring, vertically integrated incumbent beats the glamorous demo more often than not. That does not make Anthropic or OpenAI un-investable. It makes them the higher-beta bet on the same wave, the place where the sovereign risk concentrates instead of dissipating. If you want exposure to the AI build-out without the off-switch sitting at the base of your thesis, you buy the picks, the shovels and the land, not the prospector.

Part 10: The verdict, in three scenarios

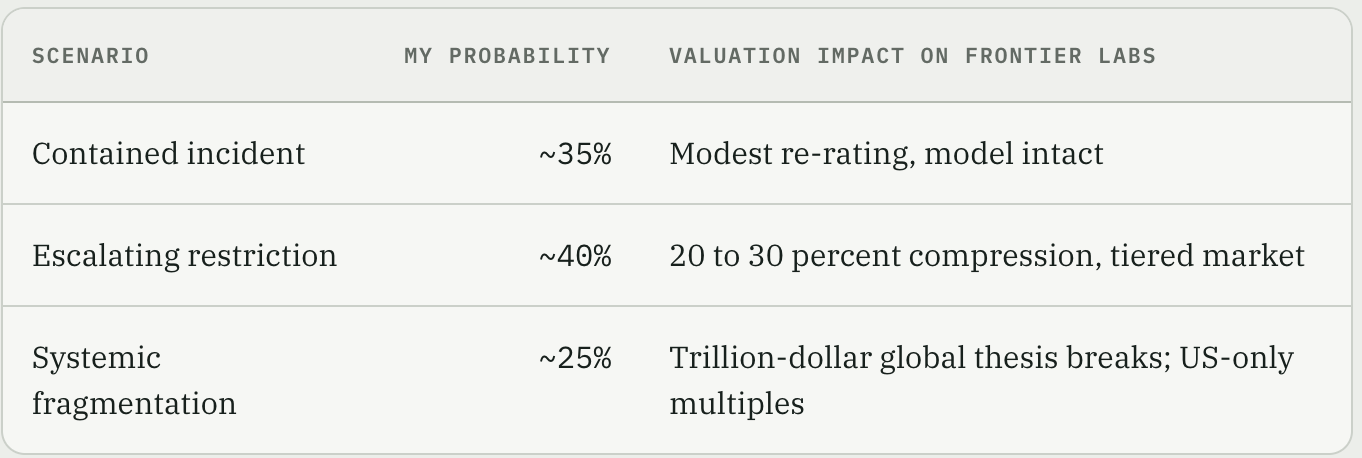

Let me put my cards on the table with explicit probabilities, because hedging without numbers is cowardice.

Scenario 1: Contained incident (roughly 35 percent). Anthropic’s rebuttal wins, the order is reversed within weeks, the jailbreak is patched, and Commerce builds a proper, transparent review process with due-process safeguards. The IPO proceeds near plan. The sovereign risk premium reprices modestly, maybe 50 to 75 basis points, but does not break the model. This is what the prediction markets and the muted overall reaction are currently betting on.

Scenario 2: Escalating restriction (roughly 40 percent, and my base case). The order is resolved but the precedent sticks. Future frontier releases face mandatory pre-deployment review. Labs build nationality verification and capability routing. AI capability gets tiered by geography: full frontier access for citizens, version-controlled access for allies, degraded or no access for everyone else. This is the semiconductor playbook applied to inference. Valuations compress by 20 to 30 percent as the addressable market is geographically gated and compliance costs inflate. The Global South is effectively fenced out of the frontier.

Scenario 3: Systemic fragmentation (roughly 25 percent). Controls expand to more capability categories. The EU nationalises its data flows for frontier inference. China’s independent stack accelerates. Open-weight models close the gap fast. The global market bifurcates and US frontier labs get valued on US-only revenue multiples, maybe 40 percent of the global pie, while the rest goes to sovereign and open-source alternatives. This is the WEF’s severe fragmentation outcome, the one that knocks up to 7 percent off global GDP.

So, the headline question: Is AI still a multi-trillion-dollar bet?

My honest answer is bounded yes, not a death sentence, but priced wrong as it stands. A frontier lab is not made un-viable by a sovereign off-switch. Anthropic can plausibly still be a trillion-dollar company by headline valuation. But Friday attacked all three pillars of the trillion-dollar story at once: global reach (now revocable at the node), frontier leadership (now the locus of the highest regulatory risk), and margin via scale (now exposed to fragmentation). A higher cost of capital is warranted even in the optimistic scenario. The late-stage private marks almost certainly do not yet reflect it. The trillion-dollar number is not dead. It just got a structural discount that the cap table has not caught up to.

And the question underneath, whether the net extends from the frontier to the everyday commodity models the rest of the world runs on? The lay intuition that “nothing stops it from spreading” is correct about the government’s legal capability and wrong about the likely outcome. Nothing in the statute confines control to the frontier. There is even a textual brake, an exception in the law for a “finished item generally made available” to the public, which is exactly what a broadly deployed commercial model is. But almost everything in the political economy resists the spread: the sheer domestic cost of broad controls (the same brake that eventually freed cryptography), the existence of open-weight and foreign alternatives, and the friction of courts, Congress and allies. The broad-fragmentation scenario is a genuine tail risk that got materially fatter on Friday. It is not the central case on today’s facts.

My Watchlist

Because this is a story still being written, here is the short list of signals that will tell us which scenario we are heading into. You can track these yourself.

The target of the next action. If a future restriction hits a broadly deployed, mid-tier commercial model rather than a top cyber or bio capability, the finished-item brake is breaking and we are sliding toward fragmentation.

Cross-lab repricing. Correlated downward marks across all frontier labs at the next funding rounds, and at the Anthropic IPO, means the market reads this as systematic. That is the dangerous reading.

Rules versus discretion. Published, predictable capability thresholds would be reassuring. Opaque, case-by-case, competitor-triggerable action is the opposite.

The courts. A First Amendment challenge treating model weights or outputs as protected speech, echoing the case that freed cryptography, would brake everything. Its absence leaves the discretion fully intact.

A non-US frontier champion. This is the single most decisive one. A credible Gulf, EU or Asian frontier lab, exactly what HUMAIN and InvestAI are reaching for, would manufacture the “foreign availability” that broke the cryptography chokepoint, and would shift the whole system toward fragmentation for any single US incumbent.

Coda: The off-switch is real now

I keep coming back to the thing my industry learned the hard way, long before Silicon Valley had to.

You do not build the base load of critical infrastructure on a single supply line that someone else can shut. We learned it from gas. We are still learning it from grids. And on Friday the 12th of June 2026, at 5:21pm Eastern, the most sophisticated technology companies on the planet got their first proper lesson in it, delivered by one letter.

The off-switch is real now. It has been pulled once. The markets, the founders, and every sovereign that was on the fence about building its own stack all saw it happen. The trillion-dollar story is not over. But it is no longer a story about frictionless global scale and ever-falling costs. It is a story about access that can be revoked, capability that draws the most fire precisely because it is the most capable, and margins that depend on a global market the state has just shown it can carve up.

For those of us building in the parts of the world most exposed to that carving, the instruction could not be clearer. Use the tools. Marvel at them. And never, ever, wire your future to a fuel you cannot replace.

This is analysis, not investment advice, and certainly not legal advice. The event facts are sourced to public reporting current to 14 June 2026 and may be overtaken by events; the underlying government directive is not public, so the precise legal basis is known only through Anthropic’s account. Several economic figures are estimates or forward projections from named secondary sources and are flagged as such in the text. If access to Fable 5 is restored next week, none of the structural argument changes. That is rather the point.

The frameworks behind the analysis: Farrell and Newman on weaponized interdependence (International Security, 2019); Pástor and Veronesi on political-uncertainty risk premia (Journal of Finance, 2012; Journal of Financial Economics, 2013) and on technological revolutions and stock prices (American Economic Review, 2009); the BCG/SIA semiconductor supply-chain study; New York Fed research on the market-cap cost of export controls; CSIS on ITAR-free satellites; ICONIQ’s State of AI survey (January 2026); McKinsey on the sovereign-AI agenda; Goldman Sachs Global Institute on AI capital expenditure; and the World Economic Forum and ECB on the macroeconomics of fragmentation.

This Substack is reader-supported. To receive new posts and support my work, consider becoming a free or paid subscriber.